The G-20 and Policy Coordination

Readers may recall that the last G20 pow-wow (see “The Gasbag Gabfest” for details) featured an uncharacteristic lack of grandiose announcements, a fact we welcomed with great relief. The previously announced “900 plans” which were supposedly going to create “economic growth” by government decree seemed to have disappeared into the memory hole. These busybodies deciding to do nothing, is obviously the best thing that can possibly happen.

Yuan, weekly – since the sharp move in USDCNY in August, market participants have begun to worry about the yuan and China’s shrinking foreign exchange reserves – click to enlarge.

There have been rumors though that they did at least strike some sort of sub rosa agreement with respect to the future course of yuan manipulation. In other words, some kind of policy coordination between China and other major currency issuers has quite possibly been agreed upon, even if only tacitly. Officially, China merely used the occasion to “reassure trading partners on foreign exchange”:

“Chinese policymakers on Thursday ruled out an imminent devaluation of the yuan as they seek to reassure trading partners ahead of the G20 summit that they can manage market stability while driving structural reforms.”

When global stock markets swooned in late August 2015 and again in January 2016, the decline in the yuan’s exchange rate was widely blamed as the cause. Considering various central bank policy decisions announced since the G20 meeting, it does appear as though a coordinated move aimed at halting the yuan’s slide and support wobbly risk asset prices has been underway.

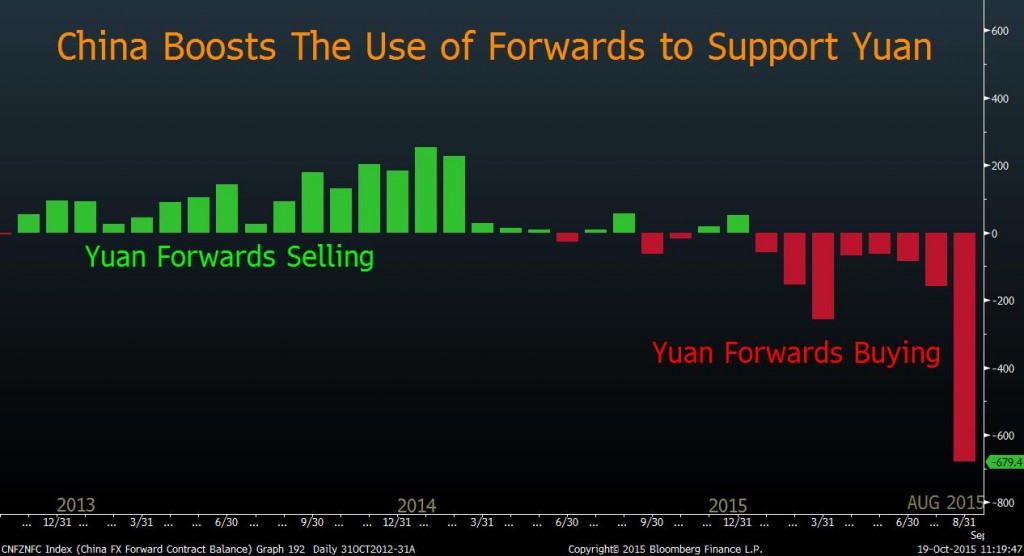

Even the Fed has become a lot more ambiguous about its previously announced rate hike plans. China’s authorities meanwhile have employed all sorts of tricks to hold the yuan up. According to Bloomberg, it has found “more discreet ways to support the yuan” – mainly by employing derivatives. Using forward transactions has two advantages from the perspective of China’s planners: they delay the official recognition of foreign exchange outflows and they don’t need to be reported to the IMF. The result is that they are “hiding the PBoC’sfootprints in the financial markets”, as Bloomberg puts it (see also Roger’s article on China’s new ways to lie with numbers).

A surge in yuan forwards buying designed to surreptitiously support the exchange rate; however, the chickens are bound to eventually come home to roost – this is only a delaying tactic – click to enlarge.

Ahead of the G20 meeting it was vehemently denied that there would be an agreement over exchange rates. China’s finance minister let it be known that such an agreement was “wishful thinking” and “a media fantasy”. However, right after the meeting we could read that “G20 Nations, Including China, Swear Off Currency Devaluations”. So there was no agreement, instead they just held a currency-related oath-taking ceremony.

Leave A Comment