In 1992, the CBOE hired Robert Whaley to develop a tradeable volatility product on equity index option prices. A year later, in 1993, the VIX was born when the CBOE started publishing real-time quotes on the implied volatility of the calculated S&P 500 index options. In those early days, I very much doubt Robert ever imagined his volatility index would someday be the cornerstone of some of the world’s most actively traded ETFs. In fact, for the next decade, no VIX instruments traded at all, and it wasn’t until 2004 that the VIX future was listed. And then, it took another five years before the first ETF based on those futures hit the exchanges. But what a ride it’s been.

Nowadays, everyone knows the VIX index. It’s no longer some arcane index reserved for derivative traders, but instead a highly liquid, easily traded way to bet on future implied volatility. And I doubt most participants realize that last part. They are not betting on current volatility. They are not betting on future volatility. They are betting on future implied volatility. Remember that point. It’s important. We’ll come back to it later.

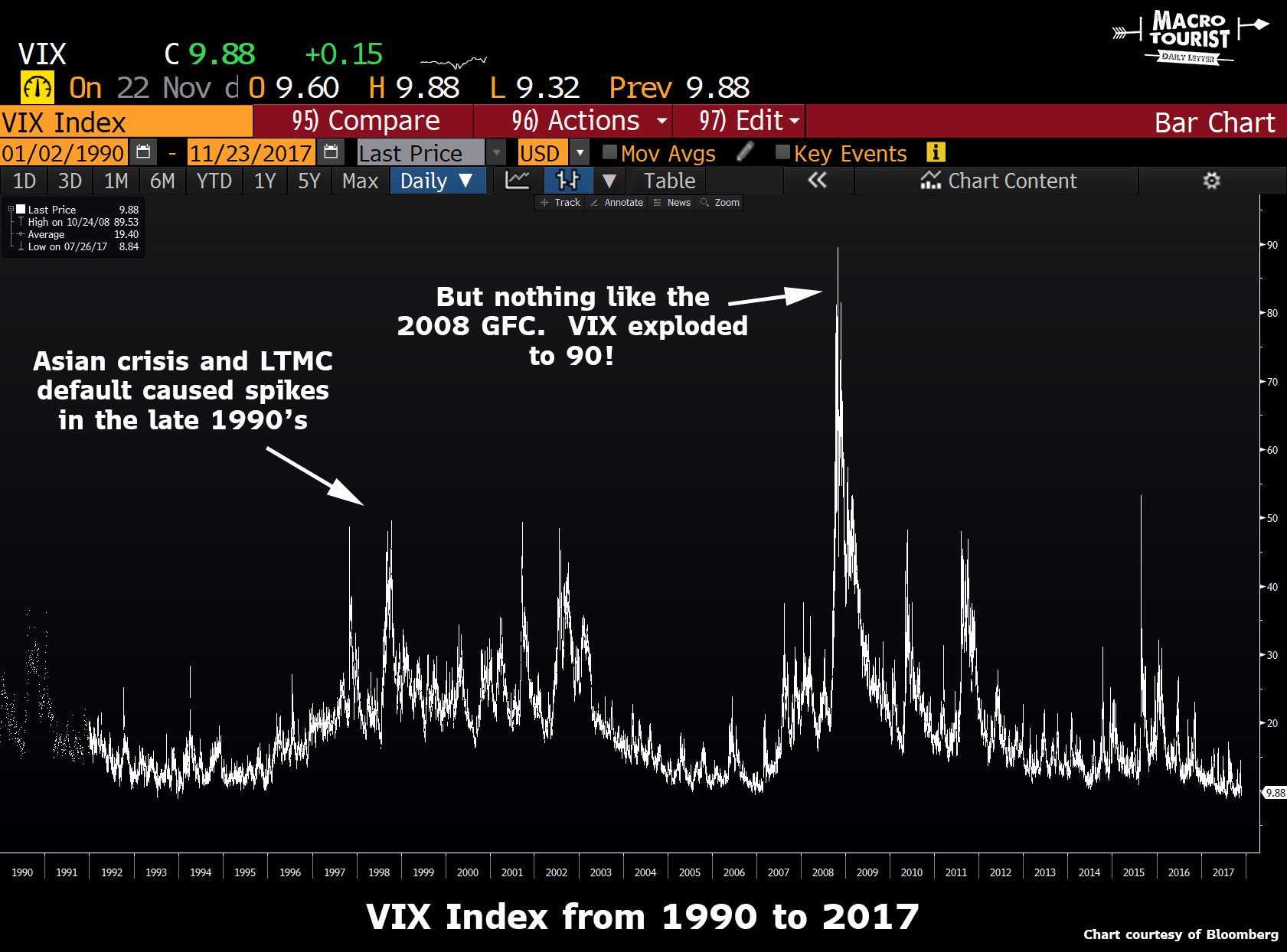

During the 2008 Great Financial Crisis, implied volatility went through the roof. It had spiked during other crises, like Long Term Capital Management and the Asian crisis, but nothing like 2008.

The Great Financial Crisis saw VIX explode to over 90. It was truly mind-boggling. The amount of future volatility the market was pricing in was unprecedented. No one trusted anyone, the financial system was imploding, and everyone was desperate to buy insurance.

And then, just like that, like all crises, it passed. But in the ensuing years, the panic might have been over, but it wasn’t forgotten. And since buying VIX had been the home run trade of the last crash, investors kept going back to VIX long positions like Lindsay Lohan goes back to the bar. So even though the actual volatility of the stock market had declined to normal levels, investors kept paying too much for the insurance, betting that future volatility would once again rocket higher.

Leave A Comment