The U.S. auto industry has been recently beset by a long list of headwinds, including global trade disputes, rising commodity prices, as well as weaker emerging market currencies.

U.S. auto giants Ford Motor Company (NYSE:F) and General Motors (NYSE:GM), for example, have generally blamed tariffs and adverse foreign exchange fluctuations for dents in their latest quarter’s earnings results.

Ford CFO Robert Shanks admitted during the company’s Q2’2018 earnings call that the quarter was “challenging,” due in part to an “increasingly uncertain” policy environment that’s “causing real unfavorable bottom line effects on the business such as higher commodity cost beyond normal cyclical effects as well as tariff-related impacts.”

Ford’s revenue, net income and adjusted EBIT were all down year-over-year in Q2’18 mainly driven by factors related to a North American production disruption at a parts supplier in the quarter, as well as ongoing challenges in the China market.

The firm’s revenue slipped by US$1.2bn from the same year-ago quarter to US$35.9bn, while its EBIT margin contracted by 3.3 percentage points to 3.2%. Furthermore, local Chinese market sales plunged in August by 36% year-on-year, and down 27% since the start of the year.

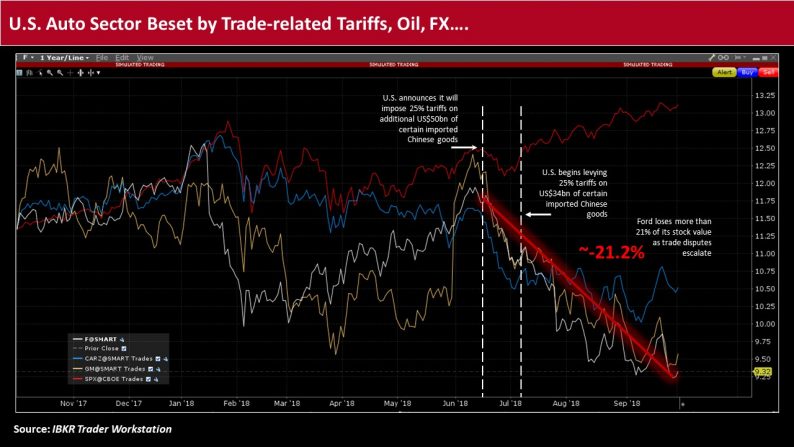

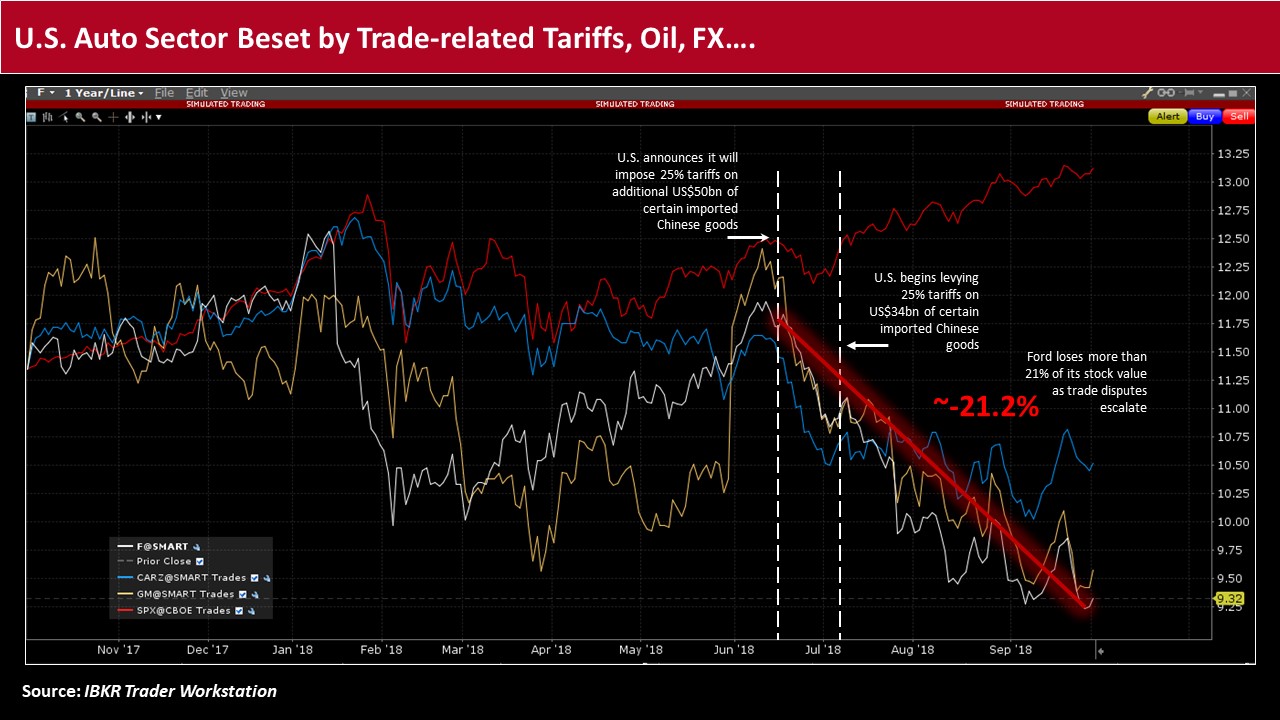

Against this backdrop, Ford’s stock has slumped more than 21% since the Office of the United States Trade Representative (USTR) announced in mid-June the imposition of an additional 25% duty on around US$50bn worth of Chinese imports containing what it deems as “industrially significant technologies,” including those related to China’s “Made in China 2025” industrial policy.

The USTR’s action, related to its Section 301 investigation, was ultimately issued in two tranches – one in early July on US$34bn worth of goods and the remainder finalized in early August.

Ford’s shares have also fallen a little more than 30% since its 52-week peak set in mid-January, while its bondholders have generally grown increasingly nervous about its credit profile.

Leave A Comment