To review our stance, which is years along now, the gold sector is not going anywhere until it becomes widely accepted that developed stock markets, including and especially those in the US, are in bear cycles. We have also drawn analogies to the Q4 2008 event that took place in what felt like a nanosecond compared to today’s long, drawn out process.For this reason, a better ‘comp’ has been the 1999 to 2001 time frame. That was a process as well.

Regardless, gold boosters viewing inflation as the reason to buy the sector are still out there pitching, but even they have retooled their pitches for a deflationary world. It is now and always has been a global economic contraction environment (assuming it eventually coerces policy makers into inflationary actions) that would be the primary driver of the next gold bull market. Say, whatever happened to all the stories about China demand, a China/India love trade, supply/demand capers on the COMEX and ‘US jobs to spur inflation driving big, smart institutional money into gold’anyway?

What happened to them is that they were debunked as having little to no bearing on the price of gold and thus, gold’s bear market.Incidentally, here is a gold-focused analyst who is a sound source of information amid the cacophony of opinions that have mostly led people astray post-2011.

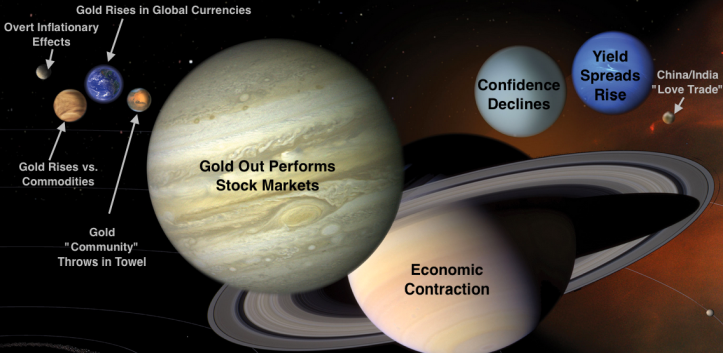

You may recall the cool graphic from the first of our Macrocosm series posted in July. What is the largest planet you see, eh Beuller? What is the second largest? Anyone?

After successfully managing the post-July process of stock market momentum loss, drop, bounce, double bottom and then rally hard (based on hysterically over bearish sentiment), and finally grinding into year-end we projected resumed bearishness, at which point it was time to gauge a new bear trend. While other indexes like those in the second chart below established bear trends ahead of time, we awaited the grand Poo bah, the S&P 500 to turn its intermediate trend negative.

Leave A Comment