Jerome Powell, the newly installed chairman of the Federal Reserve, advised in his public debut as head of the central bank that “there’s always a risk of a recession at any point in time, but I don’t see it as at all high at the moment.” Instead, he told the House Financial Services Committee that “I would expect the next two years on the current path to be good years for the economy.”

Looking two years ahead for gauging the state of the business cycle is little more than guesswork, but Powell’s comments about the current state of the US macro trend certainly align with the numbers published to date. Earlier this week, for instance, the Chicago Fed published the January report of its National Activity Index and the three month average posted a moderately high reading of +0.17, far above the -0.70 that marks recession conditions. The profile reflects a slide from the roughly +0.40 level in each of the previous three months, but recession risk remains a minimal threat, based on data available at the moment.

The Capital Spectator’s estimate of recession risk for the US also reflects a low probability for a new downturn through last month, based on a diversified set of economic indicators. Although the macro trend has cooled slightly compared with data for last year’s fourth quarter, the probability is still close to zero that a new contraction has started. (For a more comprehensive review of the macro trend on a weekly basis, see The US Business Cycle Risk Report.)

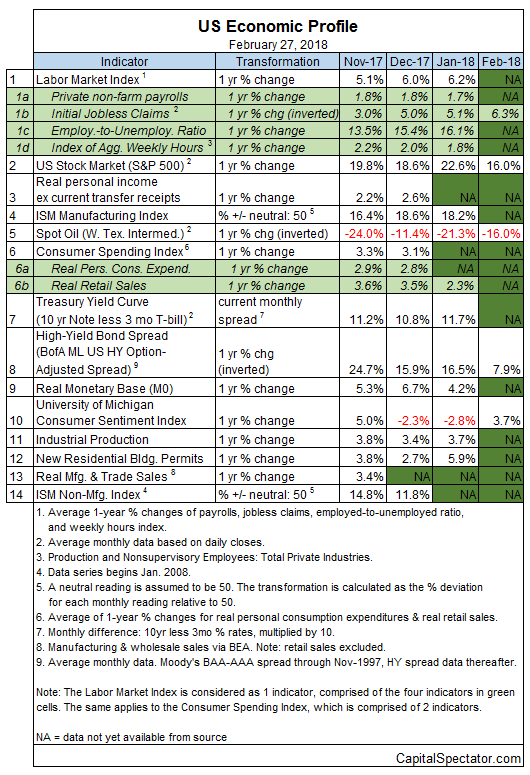

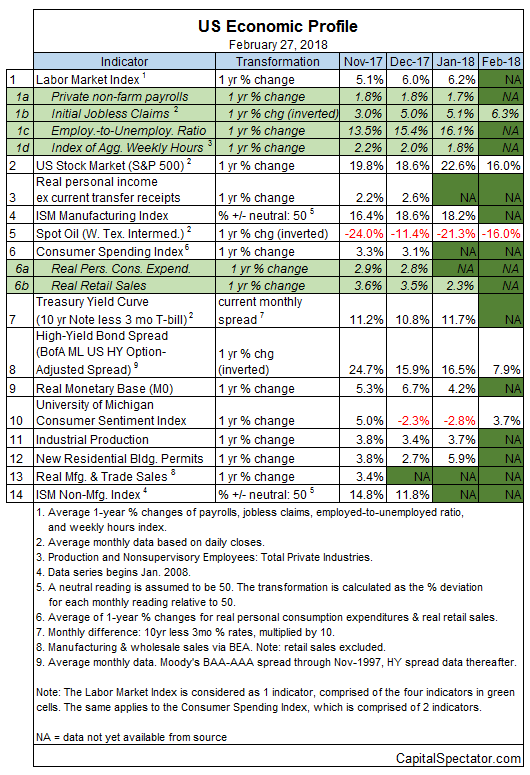

Aggregating the data in the table above continues to translate into a strong positive trend overall. The Economic Trend and Momentum indices (ETI and EMI, respectively) remain well above their respective danger zones (50% for ETI and 0% for EMI). When/if the indexes fall below those tipping points, the declines will mark clear warning signs that recession risk is elevated and a new downturn is likely. The analysis is based on a methodology that’s profiled in my book on monitoring the business cycle.

Leave A Comment