Let’s continue to look at the fiasco in the franc. We say “fiasco”, because anyone in Switzerland who is trying to save for retirement has been put on a treadmill, which is now running backwards at –¾ mph (yes, miles per hour in keeping with our treadmill analogy). Instead of being propelled forward towards their retirement goals by earning interest that compounds, they are losing principal. They will never reach their retirement goals. If you disagree, we encourage you to model it.

We say “fiasco” because living in retirement in Switzerland is like trying to live on a farm which does not grow crops. The farmer has to sell off pieces of the farm to buy groceries. As the Swiss retiree has to sell off pieces of his accumulated savings. Except the bank is also consuming his savings at -0.75%. It’s like a negative race.

Quantity Theory of Money

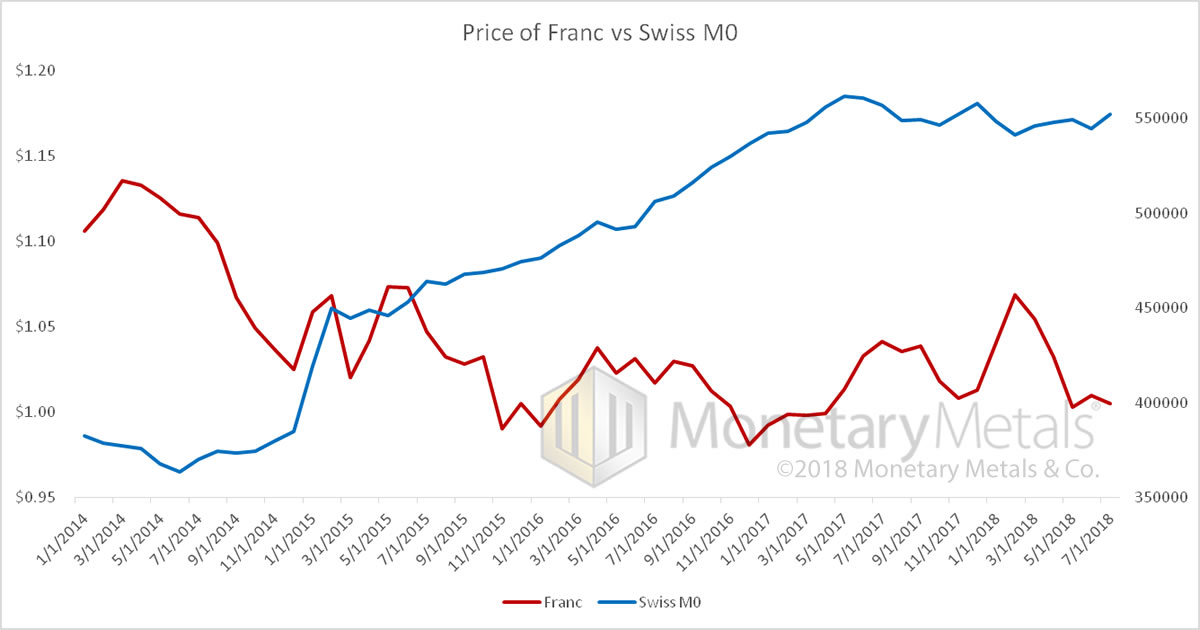

This disaster provides an interesting test of the quantity theory of money. Since mid-2013, the quantity of Swiss francs (as measured by M0) was around 380 billion. It went sideways until the end of December 2014. In January 2015, it was up to 450 billion. That move in itself, in 2-3 months, was 18%. But it first went off to the races, after that, hitting 561 billion by May 2017. In just over two years, it rose another 25%. Prices in Switzerland did not rise commensurately with these increases in the quantity of francs.

But we are interested in matters monetary. We want to see how the franc fared against the dollar, from which it ultimately derives (the US M0 admittedly rose faster during this period—44%). Here’s a graph of the price of the franc against Swiss M0.

This graph should be understood in the context of the attempt to fix the price of the franc, not against the dollar but the euro. The first part of the graph is really the trend of the euro, as the franc was fixed against that currency. But meanwhile, the market was furiously buying francs. In a vain attempt to defeat the market, the Swiss National Bank was ferociously issuing (borrowing) more. Especially in Dec 2014 and the first part of January 2015. The quantity of francs continues to increase after that through mid-2017, however, there is a little trend in the price.

The Drowning of Yield

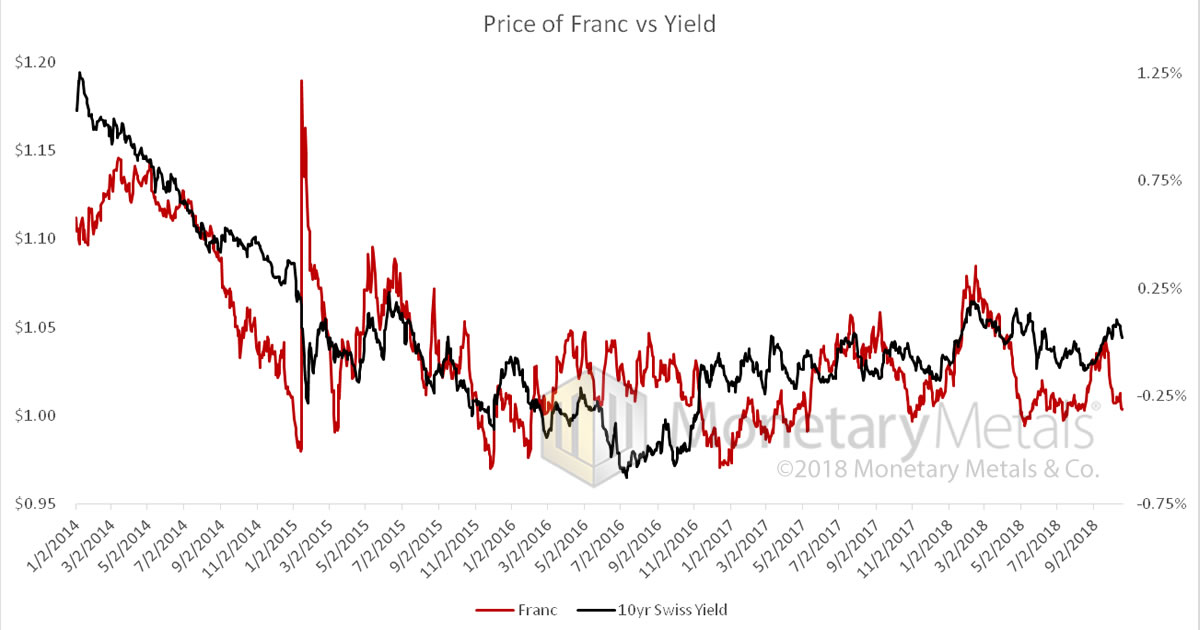

And in the breaking of this price-fixing scheme (all government price-fixing schemes inevitably break), something else happened. During the process of flooding the market with “whatever it takes” quantity of francs to keep the franc down against the euro, the interest rate was pushed negative. The yield on the 10-year bond went below zero in January 2015.

Let’s look at a graph of price of the franc against yield.

There is a much better correlation of price with yield. Why?

The lower the yield, the less attractive it is to hold and the more attractive it is to borrow, to short it, to buy another currency whose yield hasn’t gone negative yet. Like the dollar. Capital flees a currency that deals them certain losses, to friendlier climates, where a return can be made.

Leave A Comment