Wage Growth Momentum – Strong Wage Growth

In previous articles, I have discussed how strong wage growth catalyzed the increase in the 10-year yield in the past few weeks.

Technically, average hourly wage growth missed estimates on a year over year basis as it fell from 2.9% to 2.8%. But this was another strong month for wage growth once you look at the details of the report.

Month over month wage growth met estimates for 0.3% growth. The workweek length was steady at 34.5 hours.

The most important calculation for wage growth is weekly earnings. Year over year weekly earnings growth was up from 3.21% to 3.35%.

This was one of the best reports this expansion. Growth was only higher in June 2018 and October 2010. Wage growth in October 2010 is less meaningful. The unemployment rate was high; fewer workers received those gains.

We often see real wage growth weak at the end of the cycle and strong at the beginning of the cycle. Inflation overheats and then cools off. This isn’t ideal because there are fewer workers during the beginning of the recovery than the end of the expansion.

If tough comparisons prevent inflation from roaring in the next 6 months, real wage growth will explode. Nominal wage growth momentum is strong.

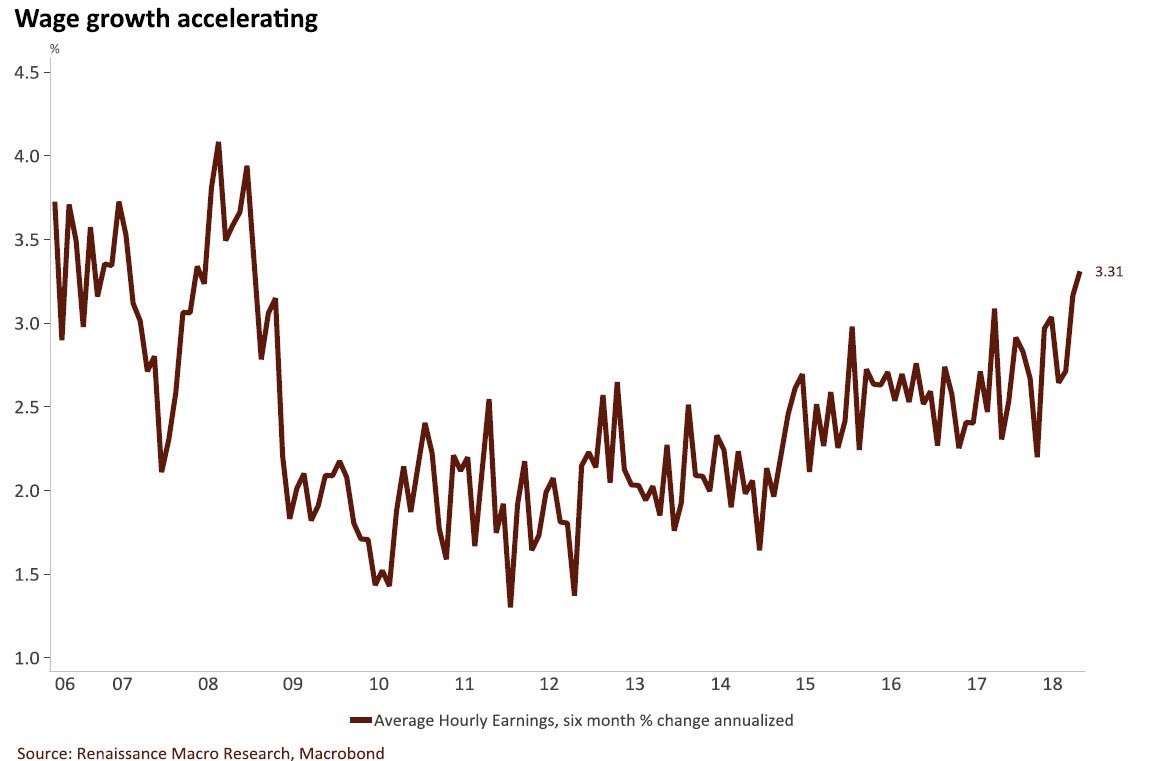

As you can see from the chart below, the 6-month change in wage growth annualized increased to 3.31%. This is the highest rate this cycle. That’s no surprise because when wage growth hit the peak in 2010, it was very volatile.

The current trend is strong and steady.

Wage Growth Momentum – Labor Force Participation Rate

The last major point to discuss about the September labor report is that the labor force participation rate was steady at 62.7%. The prime age labor force participation rate fell 0.2% to 81.8%.

This is the exact rate it was at in January. The rate bottomed in September 2015 and has gone up slowly since then. This slow increase explains why the labor market still isn’t at full employment.

Leave A Comment