As the stock market continues to press new highs, the level of optimism climbs with it. I discussed yesterday Richard Thaler’s, a recent recipient of the Nobel Price in Economics, comments about not understanding the current “irrationality of investors relating to their investing behavior.”

What is interesting is that Thaler’s received his Nobel Prize for his pioneering work in establishing that people are predictably irrational — that they consistently behave in ways that defy economic theory. For example, people will refuse to pay more for an umbrella during a rainstorm; they will use the savings from lower gas prices to buy premium gasoline; they will offer to buy a coffee mug for $3 and refuse to sell it for $6.

The fact that a man who studies the “irrationality of individuals” is stumped by current investor behavior should be alarming at the least.

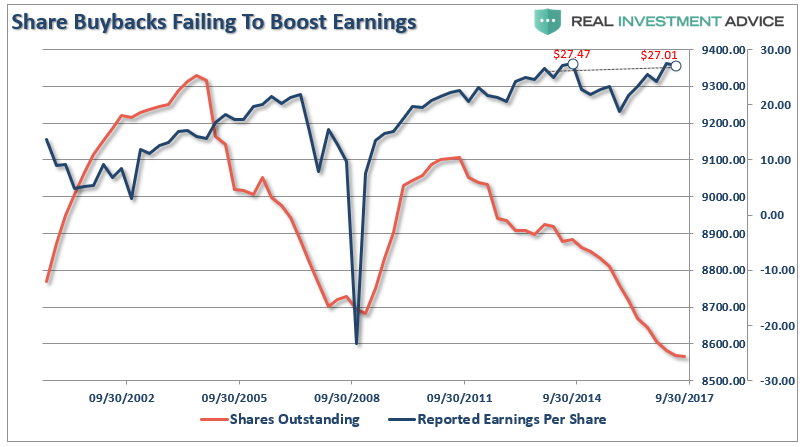

But as earnings season gets underway we once again return to quarterly Wall Street “beat the estimate game,” in which companies are rewarded by beating continually lowered estimates. Of course, the primary catalyst used to beat those estimates was not a rise in actual revenue, or even reported earnings, but rather ongoing accounting gimmickry and stock buybacks. As shown below, through the second quarter of this year, reported EPS, which includes “all the bad stuff,” actually declined in the latest quarter and has remained virtually unchanged since 2014. (But, even that is an illusion as shares have been aggressively bought back in order to sustain that same level of EPS.)

The difference between reported earnings with and without the benefit of share repurchases is substantial. The chart below shows the net difference between gross reported earnings with and without the buyback impact. Importantly, the net effect of buybacks is having less impact which, as was the case in 2007, was a precursor to the crash.

Leave A Comment