Over the last several weeks, a majority of U.S. companies have divulged their earnings. The vast majority have been their downwardly revised estimates for the first quarter with bottom line earnings per share growing at more than 18% on an annualized basis.

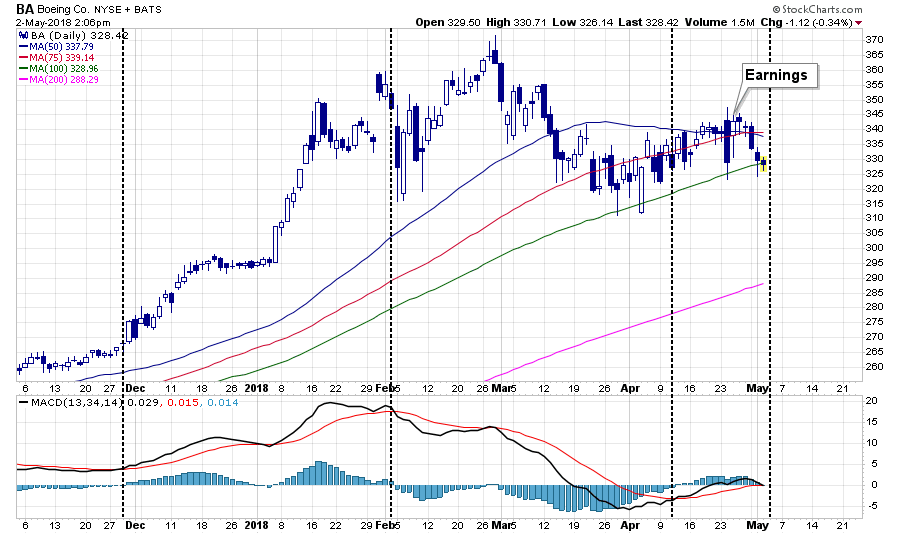

Yet, the market has failed to respond. Even stocks that have crushed earnings by a wide margin have failed to hold onto their gains in many cases like Boeing (BA).

While there are certainly bright spots to be had, the overall trend and direction of the market remains lacking. As Doug Kass noted yesterday:

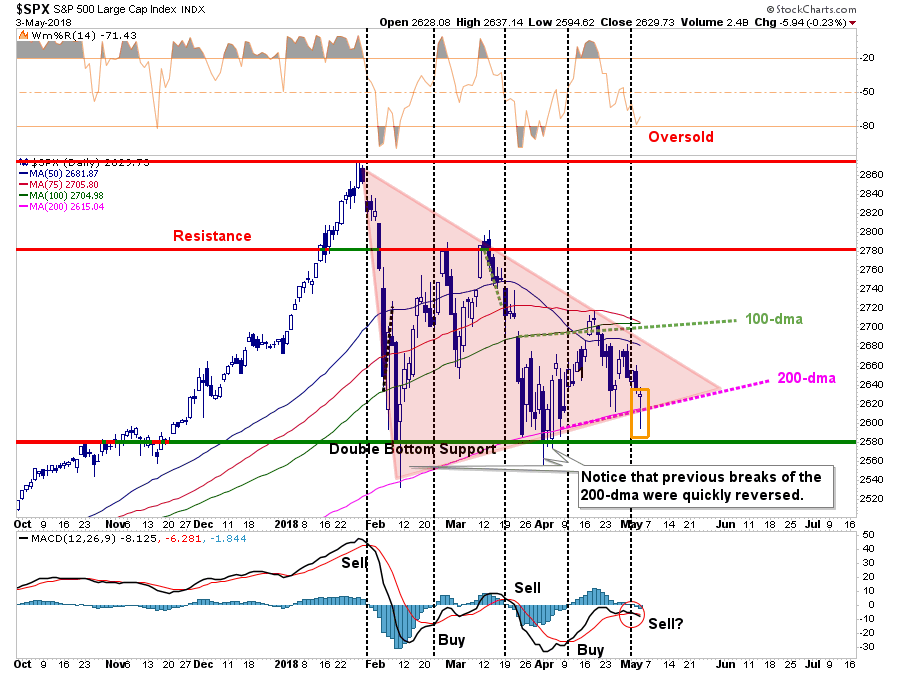

“My expectation is of a clearly defined trading range (over the near term) of the S&P Index of between 2550 and 2725. While I believe that it’s increasingly likely that we will breach the lower side of the range in the second half of this year – for now I see a continued trading range (of about 175 S&P points).”

Just a reminder…the “second half of the year” begins next month.

Stepping back we can see this direction-less trading range more clearly.

Yesterday’s “dump and pump” was led by “pretty positive comments” coming out of China relative to trade talks. The good news is the late day surge kept the markets above critical 200-day moving average support keeping bulls alive for now.

While buyers, or should I say “robots,” have repeatedly showed up to “buy the 200-dma dip,” the question is will they be able to maintain it?

The hope is that since earnings have been beating expectations the market will begin to gain some traction. However, speaking of earnings, they may not be as “organic” as they seem.

According to S&P more than $1 Trillion has gone to dividends and buybacks (exactly where we said it would go) and with Apple’s announcement of another $100 Billion the total numbers will continue to rise.

Leave A Comment