In yesterday’s post, we discussed the importance of the S&P 500 as a leading indicator of recessions in the U.S.

“The problem with making an assessment about the state of the economy today, based on current data points, is that these numbers are “best guesses” about the economy currently. However, economic data is subject to substantive negative revisions in the future as actual data is collected and adjusted over the next 12-months and 3-years. Consider for a minute that in January 2008 Chairman Bernanke stated:

‘The Federal Reserve is not currently forecasting a recession.’

In hindsight, the NBER called an official recession that began in December of 2007.”

My friend David Stockman from Stockman’s ContraCorner (a must-read site) sent me an email on Thursday morning stating:

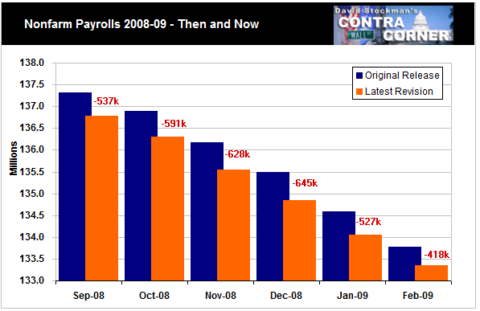

“On your topic of today regarding recession recognition, here’s another point about after-the-fact revisions. NF payrolls were revised down by about 500,000 per month during the September-February 2008 plunge:”

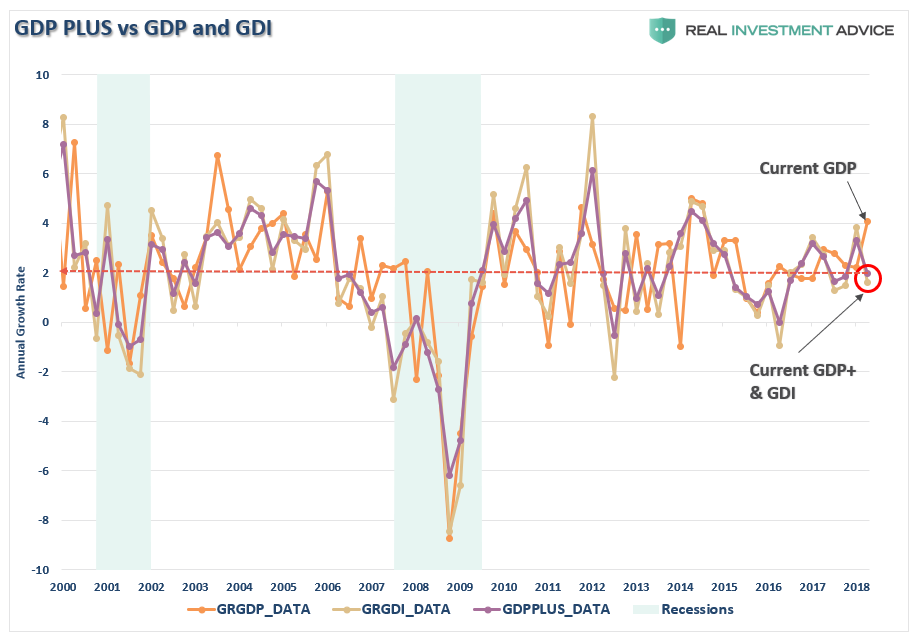

The point here is that while CURRENT economic data points are positive, there are numerous ancillary data points which suggest the economy is already weakening. My colleague, Richard Rosso, sent me this note on the Fed’s alternative GDP calculation called GDP Plus:

“GDPplus is the Federal Reserve Bank of Philadelphia’s measure of the quarter-over-quarter rate of growth of real output in continuously compounded annualized percentage points. It improves on the Bureau of Economic Analysis’s expenditure-side and income-side measures.Currently, it is showing GDP at 4.0% annual growth with both GDI and GDP-Plus running at 2.0% or less.”

Historically, when GDP has deviated above both GDP-Plus and GDI, GDP has eventually “caught-down” with the rest of the data.

Leave A Comment