“I wanted to write buy the dip, but the S&P 500 has had such a tiny drop from last week’s record high that a ‘divot’ seemed more appropriate,” Bloomberg’s Andrew Cinko wrote on Monday. Story of our life Andrew, story of our life.

There are no “dips”, anymore. There are just sporadic instances of benchmarks not closing green.

Some of this is down to the unshakable faith in the central bank put, which in the U.S. is now more of a forward guidance put than anything else – they’re normalizing the balance sheet (albeit slowly) and they’re hiking rates (tentatively), but the fact that none of that is really affecting financial conditions quite clearly suggests that the two-way communication loop between policymakers and markets has become so efficient that no one sees any utility whatsoever in trying to play for anything that even approximates a meaningful pullback.

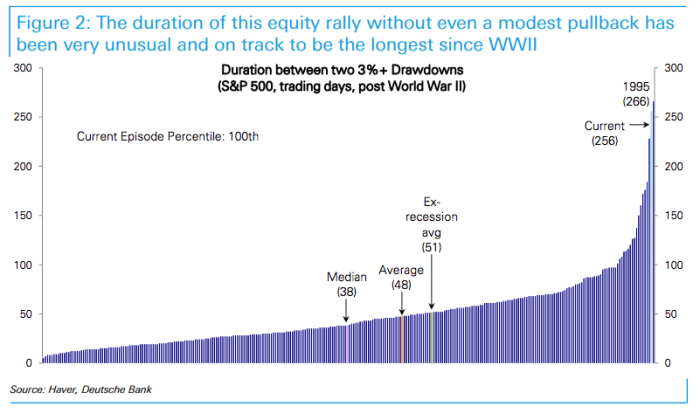

This is manifesting itself in all manner of ways, not the least of which is rapid vol. mean reversion. But the easiest way to visualize this is simply to note that if we go another two weeks without a 3% pullback, this will be longest rally since WWII:

So who’s buying the dip or, as Cinko puts it, the “divot”? Well, Deutsche Bank is glad you asked.

For one thing, the corporate bid has remained voracious. “Trailing buybacks, running currently at a massive $440bn on net have remained in line with their 3 year range,” DB writes, in a note dated late last week. Here’s the visual:

Ok, so we knew that. What else is going on? DB goes on to note that although single stock short interest has ticked up, overall short interest (i.e. including ETFs) has declined to cycle lows:

Although asset allocation funds have been trimming exposure, long/short equity fund and mutual fund exposure are both extended:

And while all of that is indeed interesting, everyone knows that when it comes to buying the f***ing dip, nobody does it like… wait for it … you.

Leave A Comment