Once upon a time, we worried about oil and other energy. Now, a song from 1930 seems to be appropriate:

Video length: 00:03:20

Today, we have a surplus of oil, which we are trying to use up. That never happened before, or did it? Well, actually, it did, back around 1930. As most of us remember, that was not a pleasant time. It was during the Great Depression.

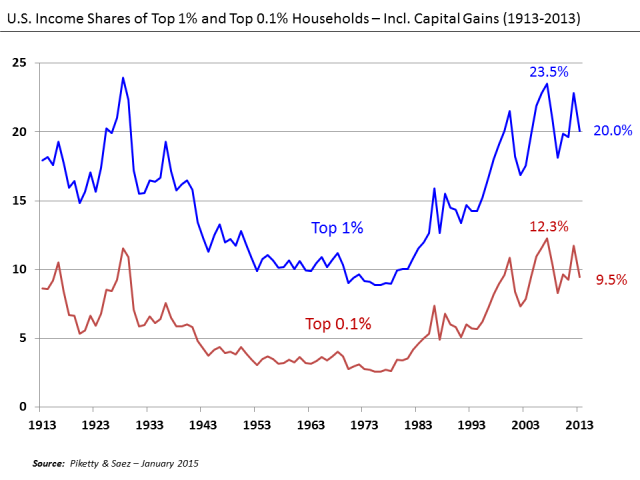

A surplus of a major energy commodity is a sign of economic illness; the economy is not balancing itself correctly. Energy supplies are available for use, but the economy is not adequately utilizing them. It is a sign that something is seriously wrong in the economy–perhaps too much wage disparity.

If wages are relatively equal, it is possible for even the poorest citizens of the economy to be able to buy necessary goods and services. Things like food, homes, and transportation become affordable by all. It is easy for “Demand” and “Supply” to balance out, because a very large share of the population has wages that are adequate to buy the goods and services created by the economy.

It is when we have too much wage disparity that we have gluts of oil and food supplies. Food gluts happened in the 1930s and are happening again now. We lose sight of the extent to which the economy can actually absorb rising quantities of commodities of many types, if they are inexpensive, compared to wages. The word “Demand” might better be replaced by the term “Quantity Affordable.” Top wage earners can always afford goods and services for their families; the question is whether earners lower in the wage hierarchy can. In today’s world, some of these low-wage earners are in India and Africa, or have no employment at all.

What is Going Right, As We Enter 2018?

[1] The stock market keeps rising.

The stock market keeps rising, month after month. Volatility is very low. In fact, the growth in the stock market looks rigged. A recent Seeking Alpha article notes that in 2017, the S&P 500 showed positive returns for all 12 months of the year, something that has never happened before in the last 90 years.

Very long runs of rising stock prices are not necessarily a good sign. According to the same article, the S&P 500 rose in 22 of 23 months between April 1935 and February 1937, in response to government spending aimed at jumpstarting the economy. By late 1937, the economy was again back in recession. The market experienced a severe correction that it would not fully recover from until after World War II.

The year 2006 was another notable year for stock market rise, with increases in 11 out of 12 months. According to the article,

Equity markets rallied amidst a volatility void in the lead-up to the Great Recession. Markets would make new all-time highs in late 2007 before collapsing in 2008, marking the worst annual returns (-37%) since the aforementioned infamous 1937 correction.

So while the stock market consistently rising looks like a good sign, it is not necessarily a good sign for market performance 6 to 24 months later. It could simply represent a bubble forming, which will later pop.

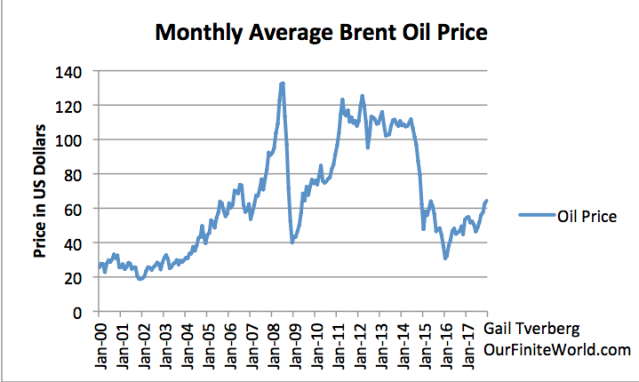

[2] Oil and other commodity prices are recently somewhat higher.

Recently, oil prices have been too low for most producers. Now, things are looking up. While prices still aren’t at an adequate level, they are somewhat higher. This gives producers (and lenders) hope that prices will eventually rise sufficiently that oil companies can make an adequate profit, and governments of oil exporters can collect adequate taxes to keep their economies operating.

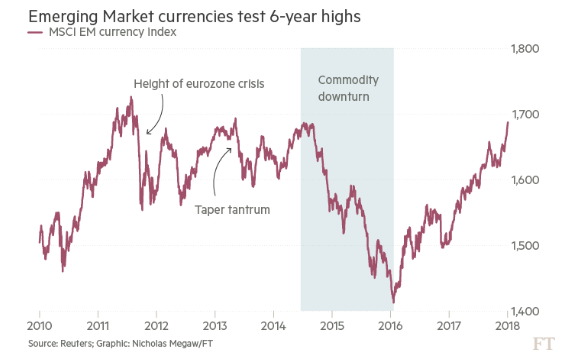

A major reason for the recent upward trend in commodity prices seems to be a shift in currency relativities for Emerging Markets.

While the currency relativities for emerging markets had fallen quite low when commodity prices first dropped, they have now made up most of their lost ground. This makes commodities more affordable in Emerging Market countries, and allows them to do more manufacturing, thus stimulating the world economy.

Of course, if China runs into debt problems, or if India runs into problems of some sort, or if oil prices rise further than they have to date, the run-up in currency relativities might run right back down again.

[3] US tax cuts create a bubble of wealth for corporations and the 1%.

With low commodity prices, returns have been far too low for many corporations involved with commodity production. “Fixing” the tax law will help these corporations continue to operate, even if commodity prices remain low, because taxes will be lower. These lower tax rates are important in helping commodity producers to avoid collapsing as a result of low commodity prices.

The problem that occurs is that the change in tax law opens up all kinds of opportunities for companies to improve their tax situation, either by changing the form of the corporation, or by merging with another company with a suitable tax situation, allowing the combined taxes to be minimized. See this recent Michael Hudson video for a discussion of some of the issues involved. This link is to a related Hudson video.

Video length: 00:14:32

Groups evaluating the expected impact of the proposed tax law did their evaluations as if the corporate structure would remain unchanged. We know that tax accountants will help companies quickly make changes to maximize the benefit of the new tax law. This is likely to mean that US governmental debt will need to rise much more than most forecasts have predicted.

In a way, this is a “good” impact, because more debt helps keep commodity prices and production to rise, and thus helps keep the economy from collapsing. But it does raise the question of how long, and by how much, governmental debt can rise. Will the addition of all of this new debt raise interest rates even above other planned interest rate increases?

Leave A Comment