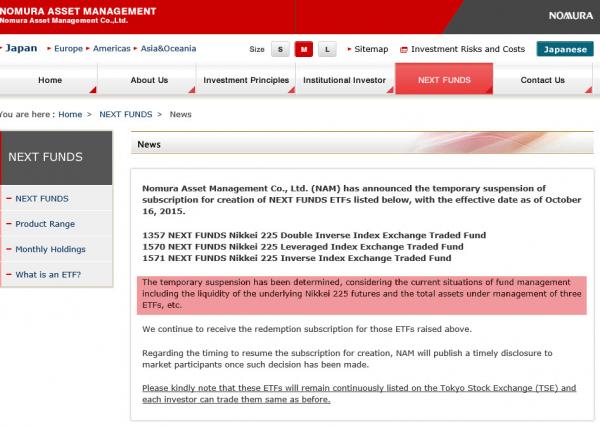

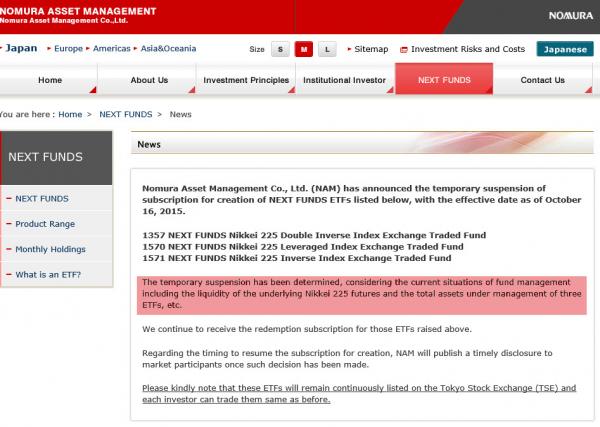

First The Bank of Japan destroyed the Japanese bond market, and then, back in May we warned that The Bank of Japan had ‘broken’ the stock market. Now, it appears the all too obvious consequences of being the sole provider of buying power in an antirely false market are coming home to roost as Nomura reports the “temporary suspension” of new orders for 3 leveraged ETFs – the largest in the world – citing “liquidity of the underlying Nikkei 225 futures market.”

Source: Nomura

As Bloomberg reported previously on Nomura’s funds,

Money is being shredded at an unprecedented rate in a souped-up exchange-traded fund tied to Japan’s most famous stock index.

Since mid-August, investors have poured a record $4.5 billion into the Next Funds Nikkei 225 Leveraged Index ETF, a security designed to rise or fall twice as fast as its namesake equity gauge. That’s too bad, considering that twice the Nikkei 225 Stock Average’s loss over that period comes out to about 21 percent.

So fast have the country’s individual investors been plowing money into the fund that even as a fifth was lopped off its price, its market value more than doubled. It’s the largest security of its kind in the world, and is now big enough to affect the whole stock market as overseers rush to buy and sell securities to meet its price target, according to BNP Paribas Investment Partners Ltd.

“They are taking up a larger proportion of the market,” said Tony Glover, head of the investment management department at BNP Paribas Investment Partners Japan in Tokyo.“Volatile markets are not great news with increasingly wider intraday swings. The funds are a big factor causing this.”

The ETF has become more popular with traders than even Toyota Motor Corp., Japan’s biggest company. Average turnover for the ETF was about 250 billion yen ($2.1 billion) a day over the past two months, triple that of Toyota.

* * *

Who could have seen this coming? Well we did… numerous times…and here is the explanation…

Two months ago, in “ETF Issuers Quietly Prepare For Meltdown With Billions In Emergency Liquidity,” we outlined the rather disconcerting circumstances that have led some large fund managers to quietly line up emergency liquidity facilities that can be tapped in the event of a sudden retail exodus from bond funds.

“The biggest providers of exchange-traded funds, which have been funneling billions of investor dollars into some little-traded corners of the bond market, are bolstering bank credit lines for cash to tap in the event of a market meltdown.Vanguard Group, Guggenheim Investments and First Trust are among U.S. fund companies that have lined up new bank guarantees or expanded ones they already had, recent company filings show,” Reuters reported at the time, in a story we suspect did not get the attention it deserved.

At a base level, these precautionary measures are the result of the interplay between central bank policy and the unintended consequences of the post-crisis regulatory regime. ZIRP creates a hunt a for yield and simultaneously incentivizes companies (especially cash strapped companies) to tap the bond market while borrowing costs remain artificially suppressed. Clearly, this is a self-fulfilling prophecy. The longer rates on risk free assets remain near, at, or even below zero, the more demand there is for new corporate issuance (the rationale being that at least corporate credit offers some semblance of yield). More demand means rates on corporate credit are driven still lower, and once yields on high grade issues get close to the lower limit, yield-starved investors are then herded into HY.

All of this supply in the primary market comes at a time when liquidity in the secondary market for corporate credit is non-existent thanks to the shrinking dealer books that resulted from the government’s (maybe) well-meaning attempt to crack down on prop trading. The result: a crowded theatre with a tiny exit.

This situation has been exacerbated by the proliferation of bond ETFs which have allowed retail investors to pile into corners of the fixed income world where they might not belong.

Leave A Comment