Medtronic (MDT) hiked its dividend by 25% earlier this year and has now increased its dividend for nearly 40 consecutive years. While MDT’s 2.0% dividend yield isn’t enough for investors living off dividends in retirement, the stock’s double-digit annual total return potential is attractive in today’s market environment, and we expect continued double-digit dividend growth in each of the next several years.

We like the diversity of MDT’s sales mix, the recession-resistant nature of its medical devices, and the company’s dominant positions in many of its key markets. With that said, we believe dividend growth investors need to have a positive view on MDT’s $50 billion acquisition of Covidien and future regulatory changes impacting the U.S. healthcare landscape before buying the stock. Let’s take a closer look.

Business Overview

MDT was founded in 1949 and manufactures a diversified portfolio of medical devices used by healthcare institutions and physicians.

The company acquired Covidien for roughly $50 billion in January 2015 to expand its presence in faster-growing emerging markets, bolster the size and scope of its portfolio of hospital supplies, and avoid some taxes by relocating its headquarters overseas. Prior to the acquisition, MDT was primarily known for its cardiac and coronary devices (e.g. defibrillators, pacemakers, valves, and heart stents), diabetes care, spinal fusion, and neural stimulation businesses. Covidien focused on hospital and medical supplies, equipment for surgeries (e.g. surgical staplers), and its vascular therapies.

The deal about doubled MDT’s revenue to $28 billion and should help it gain more leverage and prominence on hospitals’ supplier lists as they increasingly look to cut costs. Investors considering MDT should be sure they are confident in this deal because it will impact MDT (positively or negatively) for years to come.

Segments:

Through the first six months of its fiscal year 2015 (including Covidien), MDT’s sales mix by segment was: Cardiac Rhythm & Heart Failure 19%, Coronary & Structural Heart 11%, Aortic & Peripheral Vascular 6%, Surgical Solutions 18%, Patient Monitoring & Recovery 15%, Spine 10%, Neuromodulation 7%, Surgical Technologies 6%, Neurovascular 2%, and Diabetes Group 6%.

Essentially, the company’s medical device portfolio is extremely broad and diversified.

By geography, about 55% of MDT’s revenue is generated in the United States, 33% comes from other developed markets, and 12% is derived from emerging markets. Altogether, MDT’s products are used in more than 140 countries.

Business Analysis

MDT’s strength comes from its scale ($28 billion in sales), strong market positions in its key segments (#1 in diabetes, restorative therapies, minimally invasive therapies, and cardiac and vascular), and a highly diversified product portfolio.

MDT is typically first to the market with new products, a result of 50 years of innovation and a strong commitment to R&D (the company has committed to investing an incremental $10 billion in R&D over the next decade). Given the price-sensitive nature of the healthcare industry, developing successful new technologies and medical devices is essential to maintaining market share and healthy profitability.

While price seems to be an increasingly important consideration for customers going forward as a result of the Affordable Care Act (more focus on reducing healthcare costs), the mission-critical nature of many of these products can help insulate them from price pressure.

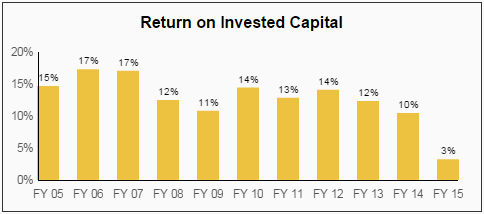

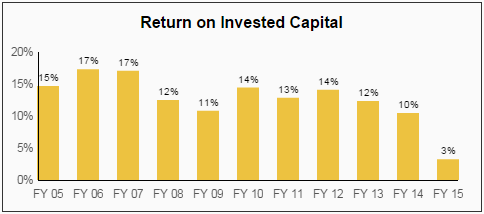

A lot of MDT’s medical devices significantly impact patients’ quality of life and must be of extremely high quality. The company’s specialized products can offer superior performance in many instances, allowing it to maintain strong market share and profitability. As seen below, MDT has maintained a double-digit return on invested capital every year (FY 15 was due to immaterial accounting distortions), suggesting it has a moat:

Source: Simply Safe Dividends

Beyond innovative products, MDT’s scale will likely serve as an increasingly important advantage as the healthcare system becomes more cost-focused and efficient. The company’s acquisition of Covidien doubled its revenue base and significantly expanded its product portfolio. MDT expects the merger to result in cost savings of $850 million annually within the next few years. Smaller medical device players could struggle to maintain their market share as MDT becomes more a low-cost, one-stop shop.

Leave A Comment