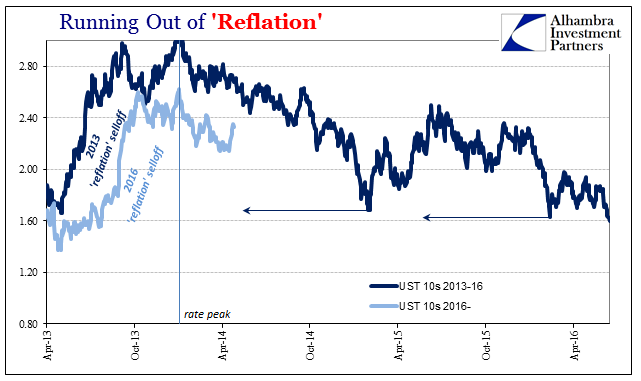

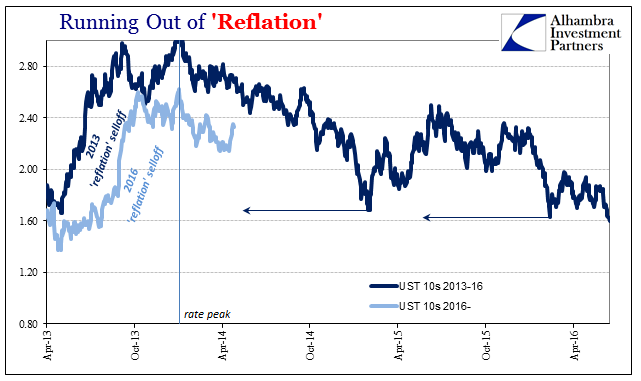

After the 2013 “reflation” selloff, it took just about two years for the treasury market to revisit (10s) the 2013 lows (rates). In all that time, each and every bond selloff was met by the same assurances that “rates had nowhere to go but up” when instead the underlying fundamentals (economy as well as money/liquidity) were the same throughout. “Rate hikes” and even balance sheet normalization are supposed to matter this time. But QE taper and then its final end was believed highly relevant, too. Maybe instead it doesn’t matter what the Fed does. Sure didn’t in 2008, so why would it in 2014, 2017, or any time hereafter?

Leave A Comment