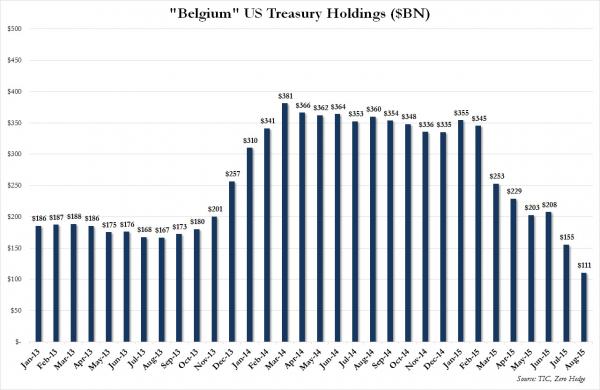

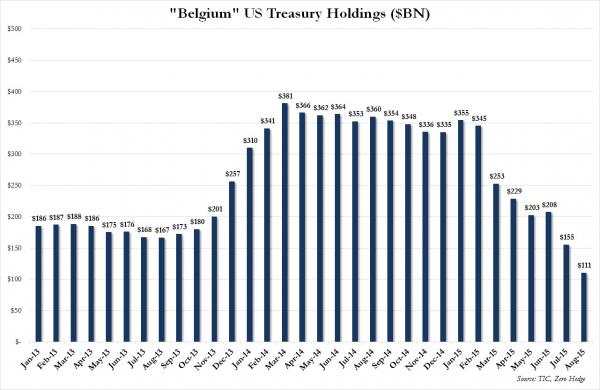

Back in May, this website was the first to explain the “mystery” behind Belgium’s ravenous Treasury buying which in early 2015 had turned into sudden selling, and which we demonstrated was merely China transacting using offshore Euroclear-based accounts to preserve anonymity. Since then theme of Belgium as a Chinese proxy has become so popular, even CNBC gets it.

Consequently, we were also the first to correctly warn that China had begun liquidating its Treasury holdings (a finding which left none other than Goldman “speechless”), which also helped us predict that China is about to announce its currency devaluation three days before it happened as the conversion of Chinese reserves from inert paper to active dollars hinted at a massive effort to stabilize the currency, and thus unprecedented capital outflows.

As a result, the only data point which mattered in yesterday’s Treasury International Capital data release was not China’s holdings, which actually “rose” $1.7 billion in the month when China actively devalued its currency and then spent hundreds of billions to prevent the devaluation from becoming an all out FX rout, but the ongoing decline in Belgium holdings. As the chart below shows, Belgium, pardon Euroclear – which is a clearing house not only for China but many other EM nations who park their reserves in Belgium – sold another $45 billion in Treasurys last month, bringing the total to a dangerously low $111 billion, down from $355 billion at the start of the year.

Lumping Belgium and China holdings into one, as we have done since May, shows that as expected, Chinese selling continued in August, and the result was another drop of $43 billion in TSY holdings in the month of August, which incidentally mirrors perfectly the previously announced decline in September Chinese FX reserves, which according to official data declined from $3.557 trillion to $3.514 trillion.

Leave A Comment