Welcome to the gates of hell, markets started Monday greeted by Cerberus as the focus for trading centered around Brexit talks stalling, German Greens gaining in Bavaria and Saudi threats to respond to pressure from EU/US over journalist Khashoggi disappearance leading to oil market jitters. However, there maybe more demons in the making with the news agenda ahead – all keeping risk-taking modest – as we face the midnight EU/Italian budget deadlines, US 3Q earnings and US retail sales.

So traders need to be more like Hercules today with plenty of labors to get over the wall of worry. Capturing the dog maybe simple in comparison to other stories yet to come. The reality of oil holding bid and CNY holding 7 are important to finding stability outside of the US. Emerging Markets remain in the crosshairs and with Asian shares sharply lower despite the US Friday bounce, its clear that trade tensions dominate fears with the Japan data modestly upbeat except in the details of mood. Similarly, China sees much the same gloom about economic prospects while inflation remains the biggest and most obvious fact for markets, witness the WPI in India today.

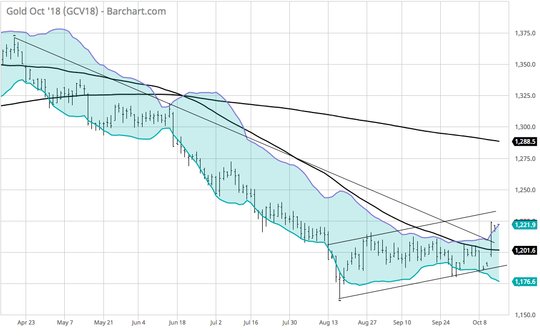

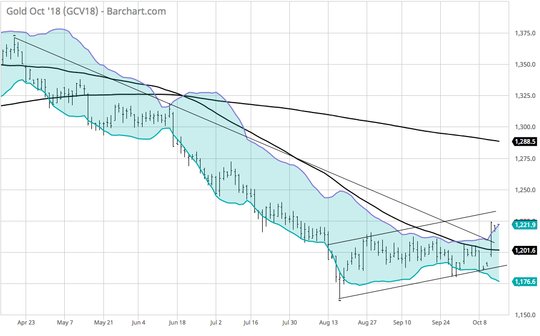

The ability for global markets to see narrowing margins – PPI-CPI being a positive number means less profits – is the key worry. Watching the markets, the safe-havens are back in play with the notable exception of the USD. We have to blame this on rates, the US/Saudi war of words and the role of China as the alternative. The notable winner today is gold and its got a larger breakout to watch at $1235. Gold maybe the best barometer to judge whether we are being dragged further into the circles of hell or we can escape for the next worry – if we break back to $1215 relax, else prepare for more trouble above $1250.

Question for the Day:Is Oil the real driver for risk? The jump in volatility last week matters as it will force smaller risk taking, hamper liquidity and make many more cautious about all asset classes. The driver for such ultimately maybe inflation concerns as the tender balancing act for markets is in the pass-through of higher prices to consumers and manufacturers. The action of central bankers to battle this into a modest rise has been the magic of the post WWII financial world. There has a notable shift this year as US rates moves up (thanks to the Fed) and the US deficit sucks out excess capital (thanks to the tax reform) all lift up off-shore USD costs. The effect on capital flows has been significant. Read the FT report from Fundamental Intelligence data on the EM capital markets in 2018.

Leave A Comment