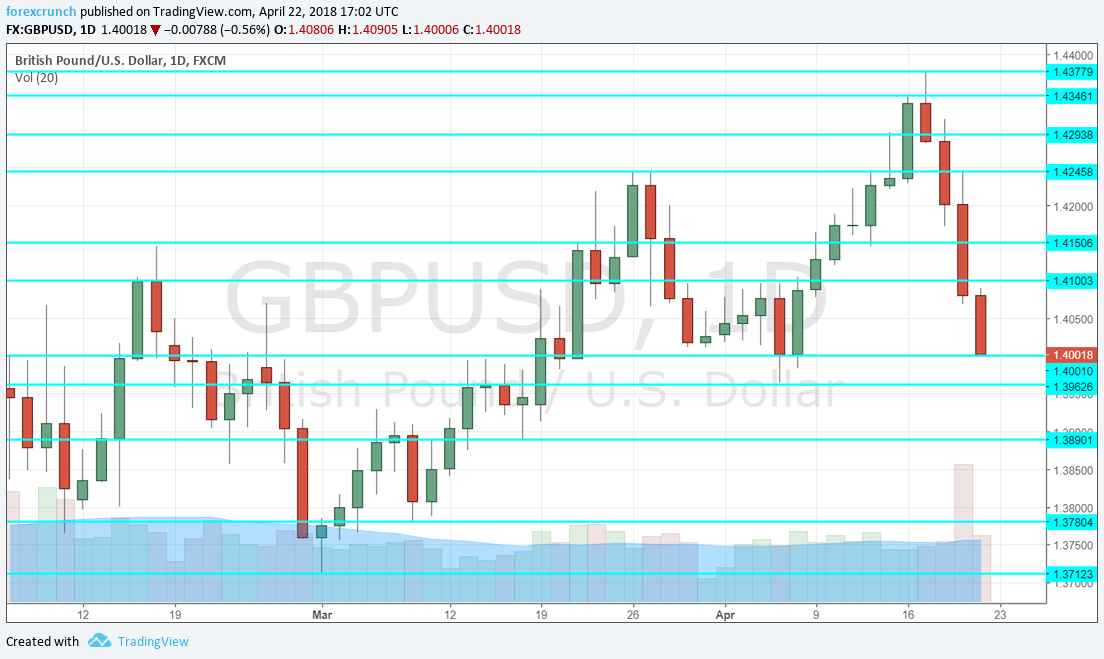

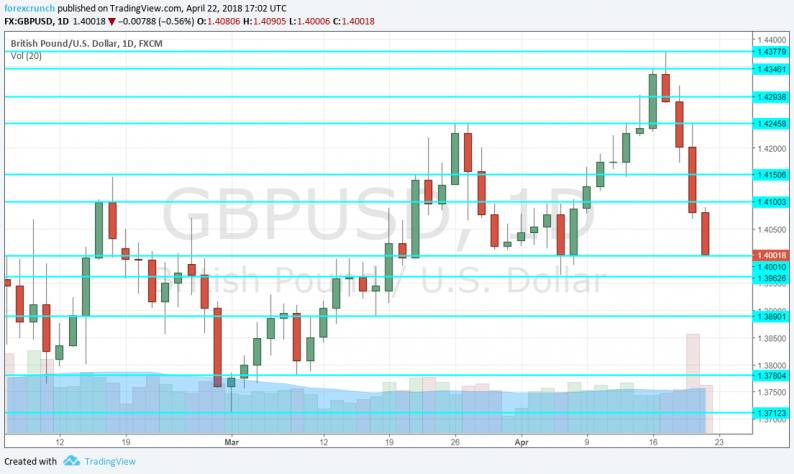

GBP/USD had a bad week when everything went wrong for the pound. After hardly holding onto 1.40, sterling now faces the GDP report and another public appearance by Mark Carney. Will it continue lower? Here are the key events and an updated technical analysis for GBP/USD.

The bad news began with wages that remained stagnant at 2.8%, short of a rise to 3% and alongside a rise in jobless claims. The second disappointment came from inflation, which fell to 2.5%, lowering the urge for a rate hike. Retail sales fell by 1.2%, double the early expectations providing the third reason to sell the pound. After the economic data came Carney’s BBC interview. He said that interest rates will rise in the next few years but hinted that the next move may not necessarily be in May. The fifth and last blow came from Brexit issues. The House of Lords voted to make changes to the Brexit Bill by a huge majority and the Irish border issue is a very thorny one without any relief so far. So, GBP/USD rose to 1.4376, the highest since June 2016, only to tumble nearly 400 pips from the highs. In the US, the dollar enjoyed higher yields, a result of good data and ongoing eagerness from the Fed to raise rates. Williams’ optimism stood out.

Updates:

GBP/USD daily graph with resistance and support lines on it. Click to enlarge:

Public Sector Net Borrowing: Tuesday, 8:30. Net borrowing by the central and local governments has been negative in February, showing a rare surplus of 0.3 billion pounds. A return to net borrowing is expected: 1.1 billion is on the cards and this may weigh on the pound.

CBI Industrial Order Expectations: Tuesday, 10:00. This survey of some 550 manufacturers has dropped to 4 points in March, a sharp drop but still a positive figure indicating increasing volume. The same number is on the cards now.

High Street Lending: Thursday, 8:30. The mortgages approved by this group represent around two-third of mortgages in the UK and the report comes out before the official one. After standing at 38.1K in February, a slide to 37.1K is on the cards for March.

CBI Realized Sales: Thursday, 10:00. The second figure from the CBI focuses on the retailers and wholesalers. After a plunge to -8 points, a small recovery to -3 is forecast. The negative number still represents lower sales volume.

GfK Consumer Confidence: Thursday, 23:01. The 2000-strong survey beat predictions in March by bouncing to -7 points. Nevertheless, it continues showing pessimism among consumers.

Nationwide HPI: Friday, 6:00. The second-earliest report on house prices has shown a second consecutive fall in the value of homes in March, by 0.2%. A bounce could be seen now.

GDP (first read): Friday, 8:30. The British economy continued growing at a rapid pace in 2016, beating other developed economies while lagging behind them in the following year. Where is it heading in 2018? After enjoying an expansion of 0.4% q/q in the last quarter of 2017, a slowdown is on the cards for Q1 2018: 0.3% q/q.

Mark Carney talks: Friday, 14:00. The Governor of the Bank of England will speak at the launch of the BOE’s econoME education program. Carney may provide further insights about the economy and perhaps a reaction to the GDP number.

Leave A Comment