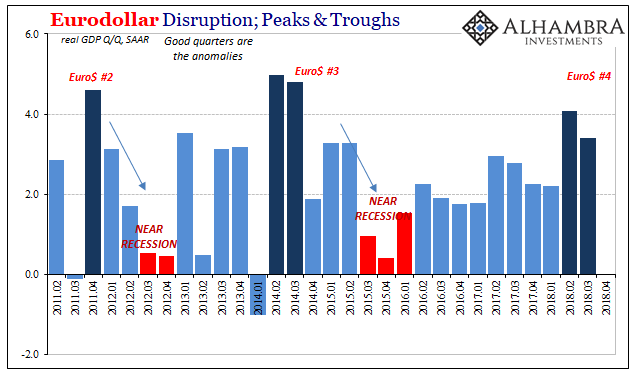

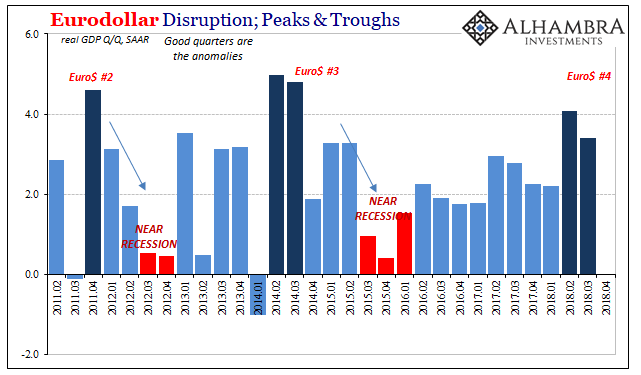

We will hear all day and for the next month (at least) about the two best quarters of GDP growth in four years. Somehow this will be used to justify calling this an economic boom, even though those two quarters in 2014 supposedly didn’t qualify. And they were better quarters, at least so far as real GDP goes.

Knee-jerk reactions are always tricky, but it’s safe to write that the bond market is thoroughly unimpressed. Treasury yields are falling despite the headline 3.5%. Struggling to understand, yet again, why anyone would bet against a resurgent US economy, commentators are first forced to acknowledge the potential for a “slowdown” already visible in many places around the world in order to postulate how this current gangbusters boom could possibly be susceptible to the “overseas turmoil”.

That’s not really the main concern. Instead, the biggest worries are right there in the current GDP report.

It gets back to the idea of globally synchronized growth. In 2017, the narrative was offered and without defining it in specific economic accounts the intuition was simple. Globally synchronized growth was supposed to convey how everything had finally changed; that, yes, the economy had posted an occasional good quarter here and there, maybe even two, in the past but starting in 2017 it was going to have good quarter after good quarter after good quarter.

This time it was different, they said.

Bonds around the world are being bid, on both already visible as well rising liquidity risk, because it’s increasingly evident it really isn’t. It’s the biggest disappointment, by far, of 2018. This is a boom except for all the trouble you don’t normally find during one. There isn’t any hint we’ve put all that sputtering behind us. Rather, combine the realization that things haven’t changed with the prospects for rising monetary and liquidity concerns and there you go.

Leave A Comment