Why Insurance Rates are Increasing

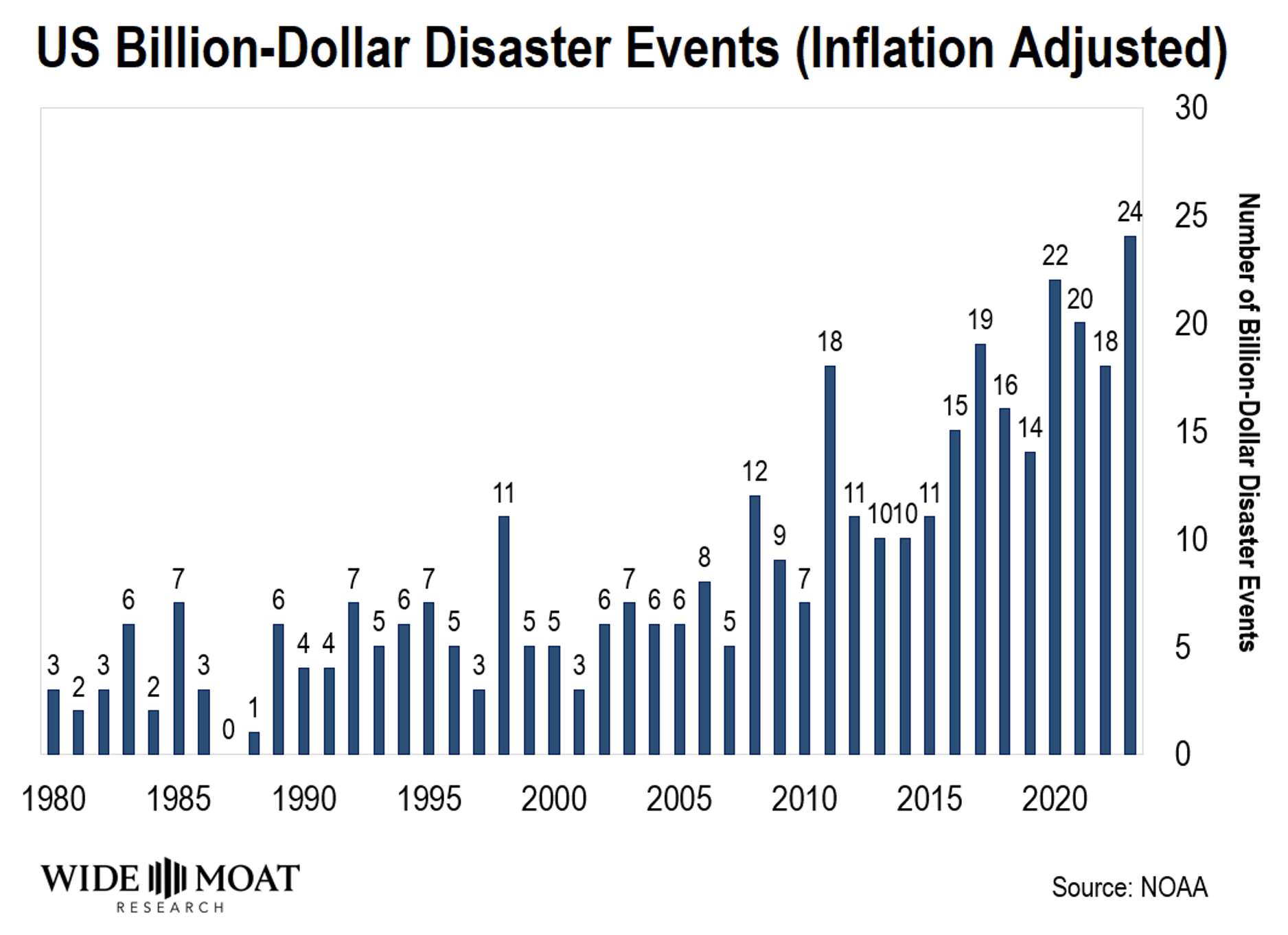

It’s not just people’s imagination. Natural disasters are happening more frequently. Up until the early 2000s, the U.S. typically had 3 to 6 “billion-dollar disasters” every year. But that changed in the last decade. Since 2011, there have been no fewer than 10 “billion-dollar disasters” every year. This year, we’ve already hit 24 — and there’s still two months left to go. And insurance companies are on the hook to pay for most of that damage.For a while, insurance companies thought it was just a fluke. Weather patterns change every year, so it might have just been a run of bad luck. They figured the weather would eventually settle down. But after a decade of increasingly frequent disasters, insurers have had enough. They’re starting to treat this as “the new normal” and are expecting disasters to keep occurring more frequently.On top of this, inflation is making things much more expensive. The cost of replacing a home increased by 55% between 2019 and 2022. In order to stay profitable with these new expectations, insurers have to raise rates. A lot. They’re also being more careful with the policies they sell.Some places are becoming “uninsurable” – with rates so high that they’re unaffordable, or no insurance companies are willing to even offer a policy. In Florida, 1 out of 6 homes has to rely on the state-backed “insurer of last resort” because there are no other options.Since 2017, eleven insurance companies in the state have been forced to close. This gives an advantage to the big insurance companies that are able to spread out their risks so that they aren’t wiped out by any one disaster. And less competition means that the remaining insurance companies are able to write more profitable policies — in other words, charge more.

This year, we’ve already hit 24 — and there’s still two months left to go. And insurance companies are on the hook to pay for most of that damage.For a while, insurance companies thought it was just a fluke. Weather patterns change every year, so it might have just been a run of bad luck. They figured the weather would eventually settle down. But after a decade of increasingly frequent disasters, insurers have had enough. They’re starting to treat this as “the new normal” and are expecting disasters to keep occurring more frequently.On top of this, inflation is making things much more expensive. The cost of replacing a home increased by 55% between 2019 and 2022. In order to stay profitable with these new expectations, insurers have to raise rates. A lot. They’re also being more careful with the policies they sell.Some places are becoming “uninsurable” – with rates so high that they’re unaffordable, or no insurance companies are willing to even offer a policy. In Florida, 1 out of 6 homes has to rely on the state-backed “insurer of last resort” because there are no other options.Since 2017, eleven insurance companies in the state have been forced to close. This gives an advantage to the big insurance companies that are able to spread out their risks so that they aren’t wiped out by any one disaster. And less competition means that the remaining insurance companies are able to write more profitable policies — in other words, charge more.

How to Profit From Increasing Insurance Rates

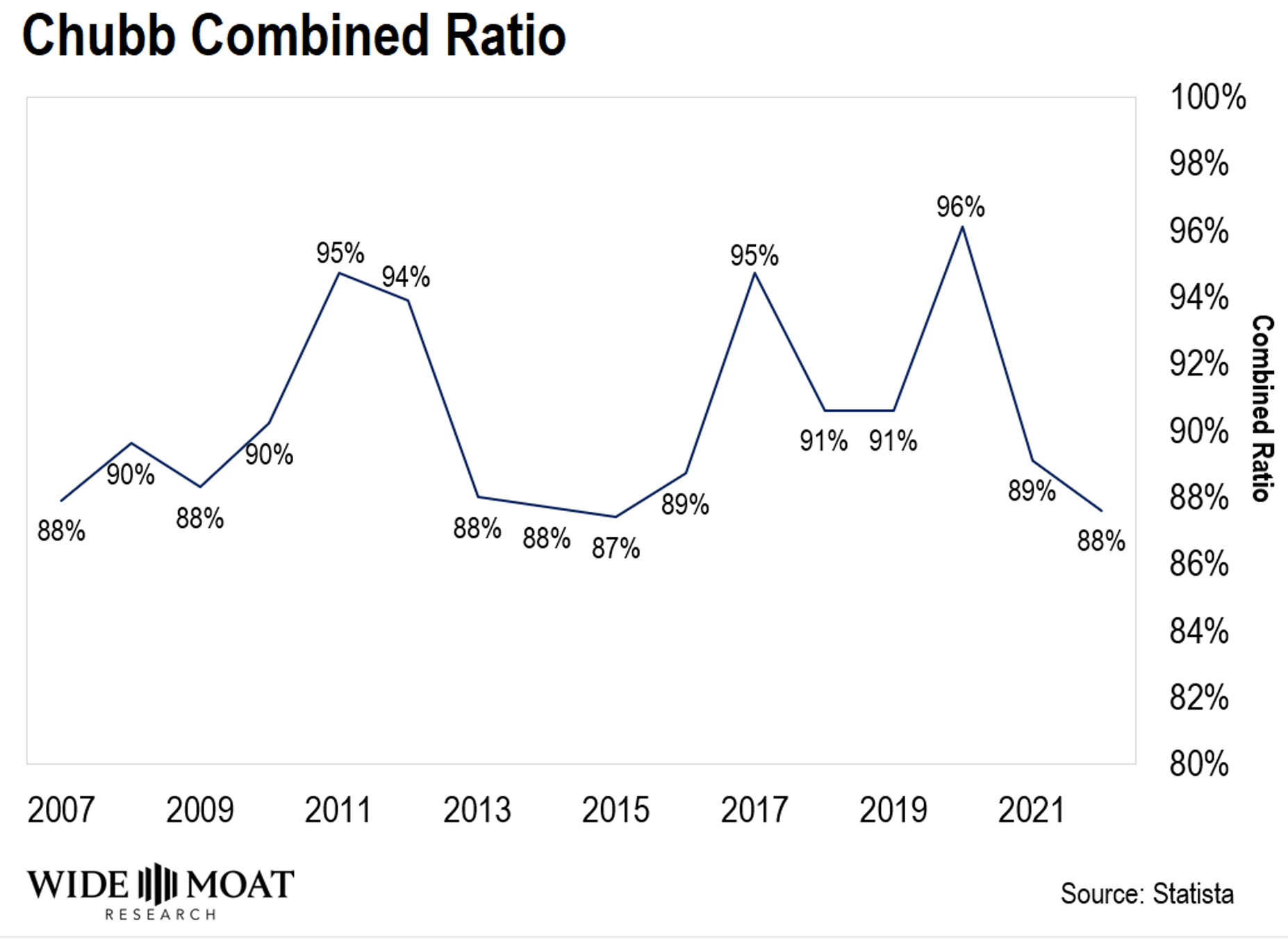

One company that stands to profit from these increasing insurance rates is Chubb Limited (CB). Chubb is the world’s largest publicly traded property and casualty insurance company. It was founded in 1882. So it has more than a century’s worth of experience in insurance. And this experience has helped the company stay consistently profitable even as disasters have increased.For the past 15 years, Chubb’s combined ratio has remained around 90%. And if you’re wondering what that means, an insurance company’s “combined ratio” shows how much of the money it gets through premiums is used to pay claims and run the company.A combined ratio over 100% means the company is losing money on its insurance policies. Insurance companies with lower combined ratios are more profitable. And even in years when the company had to pay out more claims due to disasters, its combined ratio has never gone over 100% as you can see below. So as insurance rates go up, Chubb will be able to keep its combined ratio low and its profits high. Chubb also benefits from rising interest rates. That’s because it has a large amount of insurance “float.” Float is one of the reasons Warren Buffett was so successful with Berkshire Hathaway. This is how he described it in his 2010 letter to shareholders:

So as insurance rates go up, Chubb will be able to keep its combined ratio low and its profits high. Chubb also benefits from rising interest rates. That’s because it has a large amount of insurance “float.” Float is one of the reasons Warren Buffett was so successful with Berkshire Hathaway. This is how he described it in his 2010 letter to shareholders:

“Insurers receive premiums upfront and pay claims later… This collect-now, pay-later model leaves us holding large sums – money we call ‘float’ – that will eventually go to others. Meanwhile, we get to invest this float for Berkshire’s benefit.”

Chubb invests most of its float in low-risk bonds. Right now, the yield on its portfolio is around 3.4%. But as those bonds mature, Chubb can reinvest the money into higher yielding bonds at approximately 5.8%. That means its investment income will keep rising as interest rates go up.Chubb shares yield 1.7%. And the company is a reliable source of growing income – it has raised its dividend every year for the past 30 years. Over the past three years, the S&P has returned 29%. In that same time, Chubb has returned 71%.And Chubb shares are still a good bargain. They trade at 11.1x earnings. That’s 10% below their long-term average of 12.4x earnings. And the company’s earnings will get a strong boost from rising insurance premiums and high interest rates in the years to come.So if you want to profit from increasing insurance rates, Chubb is a great option for your portfolio.More By This Author:Why This Drugstore Will Avoid Rite Aid’s Bankruptcy FateThe Office Sector Looks Like It’s Making A ComebackHow Consumer Goods Will Survive the Negative Impacts of Ozempic

Leave A Comment