Earlier in the week we noted the ‘odd’ surge in downside protection demand

even as tech stocks were soaring, and now JPMorgan is noting the S&P has shifted to a large ‘negative gamma’ underhang which “could boost volatility if we were to sell off.”

As Bloomberg notes, options markets suggest a lack of confidence in the rally. Traders are piling into downside hedges on every uptick in prices…

And JPMorgan derivatives desk writes:

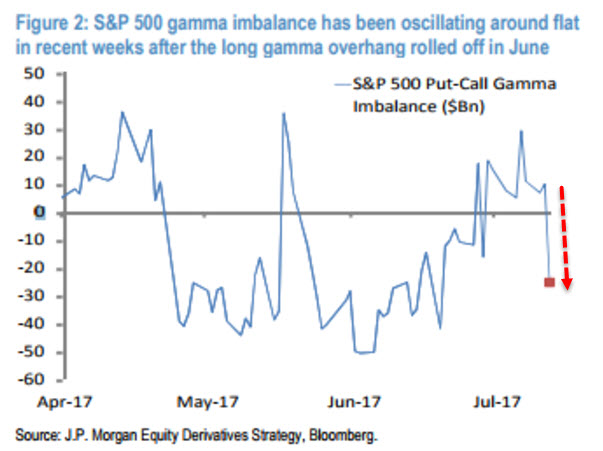

Equity realized volatility increased moderately since June expiry (e.g. 15-day S&P 500 volatility increased from 4.5% to 9%), in line with our view, as much of the long gamma overhang heading into June rolled off.

The market has been oscillating around the level where the P-C gamma imbalance is flat (Figure 2) over the past few weeks.

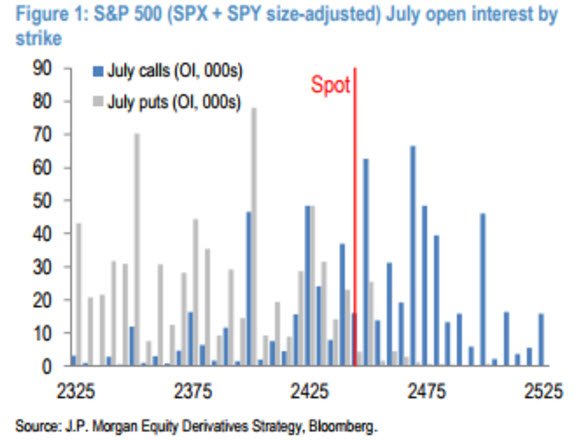

Next Friday ~$550Bn of S&P 500 options are set to expire.

We note sizeable outstanding call positions on the 2450-2480 strikes which could lead dealer hedging to dampen market volatility next week should the market trade near/in this range…

…and large put positions on the 2370-2400 strikes that could boost volatility if we were to sell off.

As a reminder, JPMorgan colleague Marko Kolanovic’s recent volatility conclusion suggests this won’t end well:

“we think current low levels of volatility is not a new normal and will not last very long given the amount of leverage, rising rates, and the approaching reduction of central bank balance sheets.”

Hopefully, that settles that.

But if indeed passive investors and systematic, quant strategies “never sell”, and rarely react to underlying shock factors, will the market just grind on forever? The answer to that emerges from Kolanovic’ explanation of the May 17 selling, and why there was no follow through:

As macro quantitative investors (including dynamical hedging programs) are a potential driver for a selloff, it is important to understand what is driving them. Relevant signals are price momentum for trend followers, bond-equity correlation for volatility targeting and parity strategies, and intraday market volatility for a broad range of hedging and dynamic risk management strategies. Our readers will notice that we did not call for the May 17th event to trigger a broader selloff. The reason that none of the triggers for systematic selling were breached. Momentum stayed solidly positive, and the rally in bonds almost entirely offset equity selloff for investors that run high bond allocations. Additionally many volatility targeting strategies have already reached leverage caps at higher levels of volatility (than what was achieved on May 17th).

Option positioning going into May 17th was also benign. Our estimates of market making positions at the start of the day were heavily long gamma (~$35bn C-P) – initially buying into the market weakness. After ~120bps decline, these positions turned short mid-day and drove the market by additional 60bps lower into the close. As it happens most of the time, this 60bp move reverted the following day (Figure 3).

Leave A Comment