That the velocity of money has been crashing while the money supply has been exploding doesn’t seem to bother the mainstream pundits. There is always a fancy-footwork explanation of why whatever is crashing no longer matters.

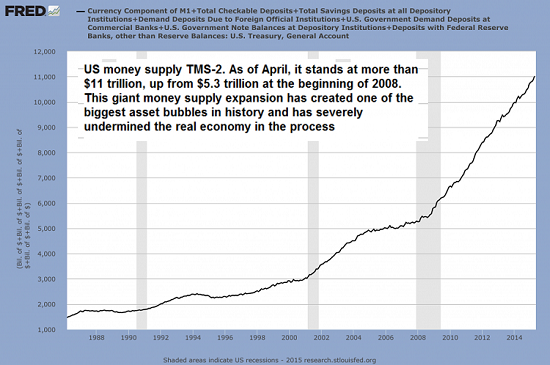

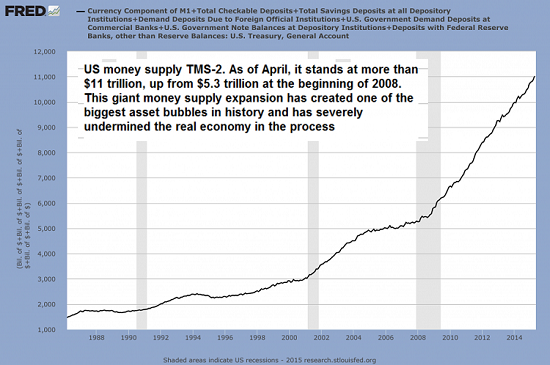

Take a look at these two charts and tell me money velocity doesn’t matter. First, here’s money supply: notice how money supply leaped from 2001 to 2008 as the Federal Reserve pumped liquidity and credit into the economy, and then how it exploded higher as the Fed went all in after the Global Financial Meltdown.

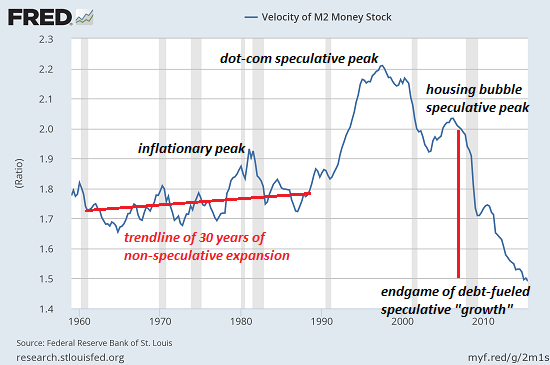

Now look at a brief history of the velocity of money. There are various measures of money supply and various interpretations of velocity, but let’s set those quibbles aside and compare money velocity in the “golden era” of the 1950s/1960s and the stagflationary 1970s to the present era from 2008 to 2015–the era of “growth”:

Notice how the velocity of money remained in a mild uptrend during both good times and not so good times. The inflationary peak of 1979-1982 (Treasury yields were 16% and mortgages were 18%) generated a spike, but velocity soon returned to its uptrending channel.

The speculative excesses of the dot-com era pushed velocity to unprecedented heights. Given the extremes in velocity, it is unsurprising that it quickly fell in the dot-com bust.

The Federal Reserve launched an unprecedented expansion of money, credit and liquidity that again pushed velocity up in the speculative frenzy of the housing bubble. But note that despite the vast expansion of money supply, the peak in the velocity of money was considerably lower than the dot-com peak.

Since the collapse of that speculative bubble, the Fed’s all-in expansion of money, credit and liquidity has failed to stem the absolutely unprecedented collapse of money velocity. Clearly, expanding money, credit and liquidity no longer generates any velocity.

Rather, the inescapable conclusion is that Fed policies have effectively crashed the velocity of money. How is this possible?

Leave A Comment