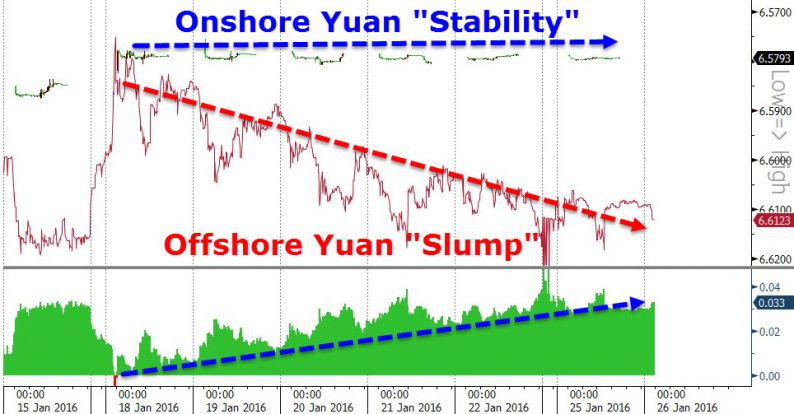

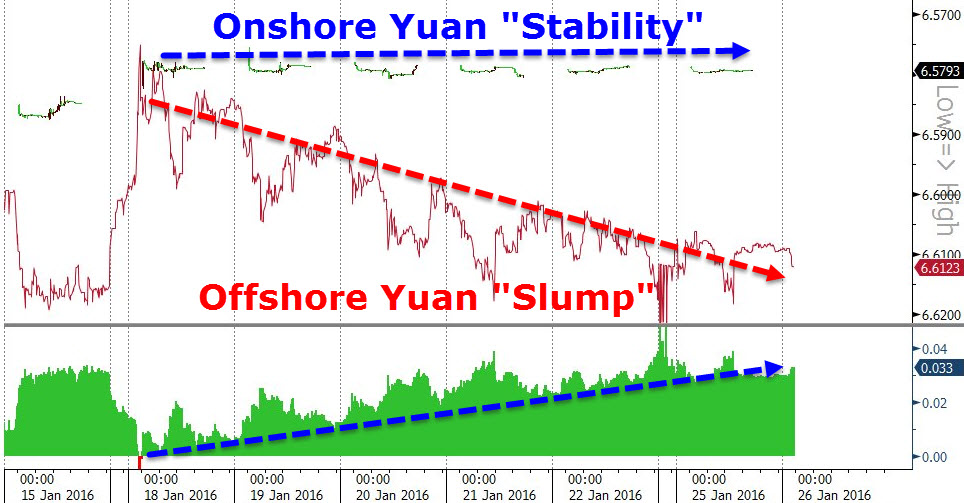

Following the afternoon weakness in US equities, Offshore Yuan has been limping lower into the fix, not helped by comments from a MOFCOM researcher that “China is able to withstand currency fluctuations” implicitly warning carry traders to stay away and suggesting the dollar’s dominance would not last long. CNH is now at 3-week lows against CNY, over 300pips cheap – which prompted the major short squeeze last time. Chinese stocks are modestly lower but more worrying is the 7-day slide in Chinese corporate bond yields – the most in 2 months – hinting perhaps that the last bubble standing is bursting.

Having dismissed calls for large scale stimulus, the Year-end liquidity spigot is wide open…

Consisting of 360bn 28-day and 80bn 7-day reverse repo.

As PBOC held the Yuan Fix “stable” for the 13th day in a row.

Offshore Yuan continues to weaken and diverge from the “relative” stability of onshore Yuan as MOFCOM resercher Mei Xinyu writes that China is willing and able to stand temporary fluctuations in currency rates to gain independence of its monetary policy,. adding that the Yuan couldn’t be pegged to dollar perpetually since China is the 2nd largest economy in world and a strong position of dollar won’t last long.

Is it us or does that sound a little more like a threat to dollar hegemony than a warning about volatility?

Chinese CDS continue to confirm Offshore Yuan’s implied weakness – the last time CNY remained “stable” in the face of devaluation stress like this was in the pre-amble to August’s collapse…

Finally, we draw attention to the fact that the “last bubble standing” – Chinese corporate bonds – appear to be cracking, having seen yields increase for the last 7 days – the most since mid November…

Leave A Comment