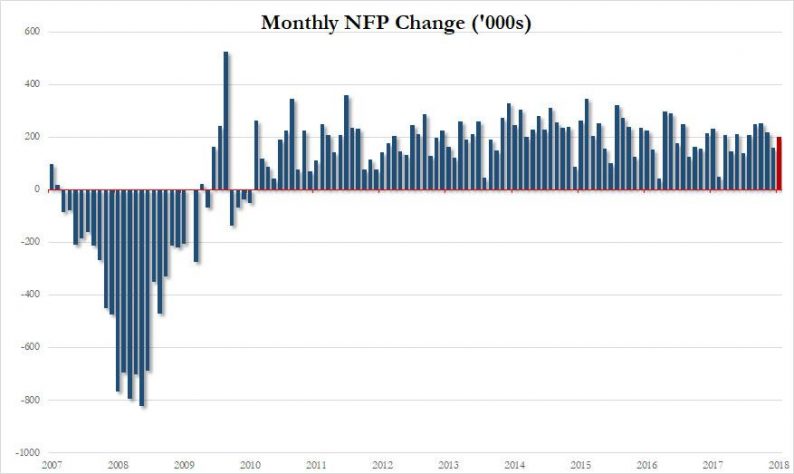

While Wall Street did expect a whisper number above the consensus forecast of 180K, the big question for today’s payrolls report was what would average hourly earnings – that critical leading indicator for inflation – do. Well, according to the BLS, while January payrolls did indeed beat, rising by 200K, above consensus…

… it was the average hourly earnings that slammed expectations, rising by 2.9% Y/Y (and up 0.3% M/M, exp. 0.2%) well above the 2.6% expected, and the highest print since Jun 2009.

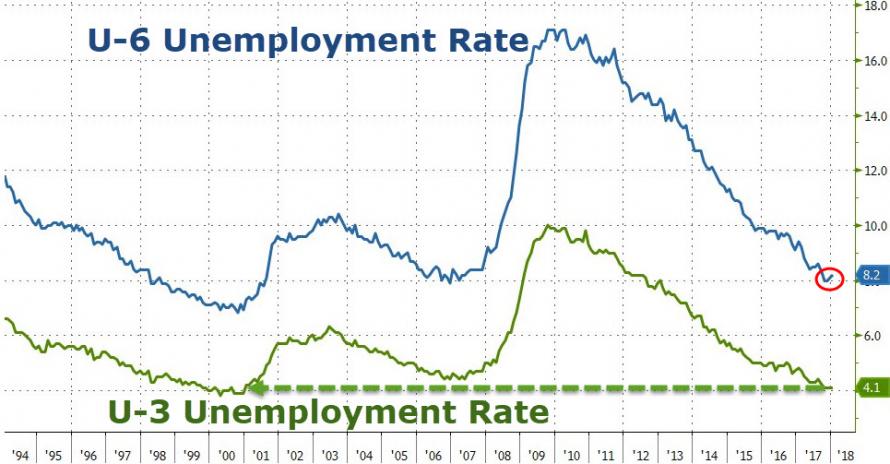

The unemployment rate, meanwhile, kept constant at 4.1%, as expected.

Going back to payrolls, the change in total nonfarm payroll employment for November was revised down from +252,000 to +216,000, and the change for December was revised up from +148,000 to +160,000. With these revisions, employment gains in November and December combined were 24,000 less than previously reported. After revisions, job gains have averaged 192,000 over the last 3 months.

In kneejerk response, Bill Gross just said that the jobs report “should send the 10Y yield to 3%”, and the report ensures the “Fed will continues to hike.”

Summarizing the report’s key details:

Some additional details:

Total nonfarm payroll employment rose by 200,000 in January. Employment continued to trend up in construction, food services and drinking places, health care, and manufacturing.

Leave A Comment