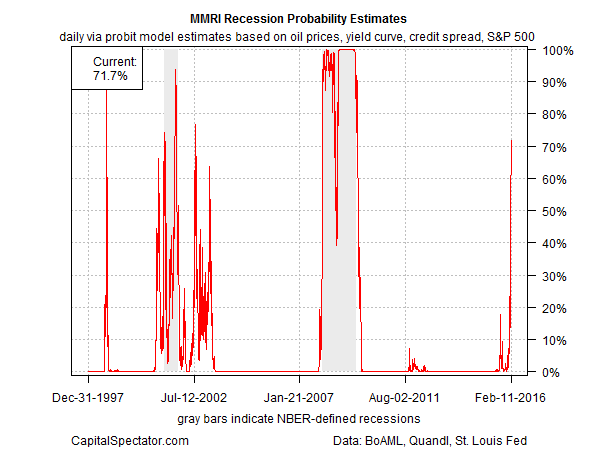

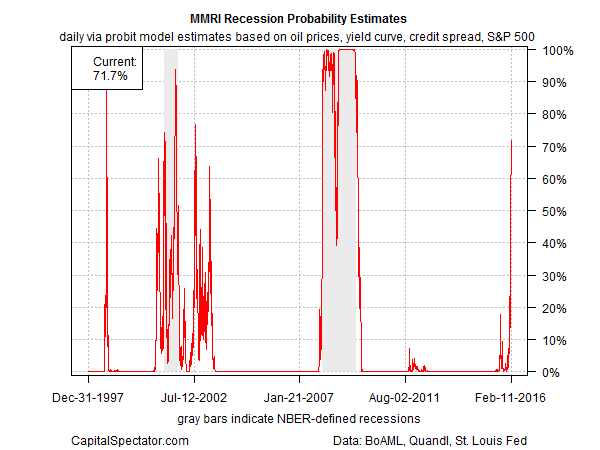

The battle between macro and markets rages on. Yesterday’s update of the ADS Index—a US business-cycle metric published by the Philadelphia Fed—remained comfortably in growth territory, in part due to yesterday’s upbeat report on jobless claims (one of the index’s six components). A markets-based estimate of the US economic trend, by contrast, continues to price in a new recession, based on the Macro-Markets Risk Index (MMRI), which aggregates four corners of the financial and commodities realm in an effort to gauge the crowd’s outlook. (See here for MMRI’s design details.)

The standoff leaves investors with a difficult question: embrace the market’s grim forecast or reserve judgment and wait for confirmation—or rejection—via the hard economic data? Most of the time the two sides of this coin are in alignment. But current conditions have dispensed an awkward state of affairs. Indeed, the MMRI’s implied recession probability via a probit model ticked higher yesterday, reaching nearly 72%–the loftiest reading since 2009, when the previous downturn was winding down.

History shows, however, that market-based estimates of recession risk can be wrong. Markets go into hissy fits for a variety reasons, and so it’s always unclear in real time if the return of dark signals in the crowd’s composite pricing preferences are a warning sign for the economy overall or a lesser evil.

The Philly Fed’s ADS Index continues to favor the latter view. Indeed, boosted by the latest decline in the weekly jobless claims data the current ADS value stands at roughly -0.15. That’s still well above the -0.80 reading (horizontal red line in chart below) that’s considered an “optimal recession threshold), based on a study by the San Francisco Fed (“Diagnosing “Diagnosing). By that standard, there’s still a comfortable margin between current levels of US economic activity and the tipping point for the ADS Index that marks the start of a new recession.

Leave A Comment