There is just something about August. It is irresistible, apparently, in all the wrong ways. For starters, there are big ones and small ones but somehow they all line up against liquidity and plentiful eurodollar money. In the former class, there was, of course, August 9, 2007, August 9, 2011, and August 10, 2015. Even in the latter category, there was August 28, 2013.

If July was a reasonably calm month if only by contrast to April and May, August less than halfway through is proving the “dollar’s” larger move (not “weak”). I wrote last week about this deflationary decade:

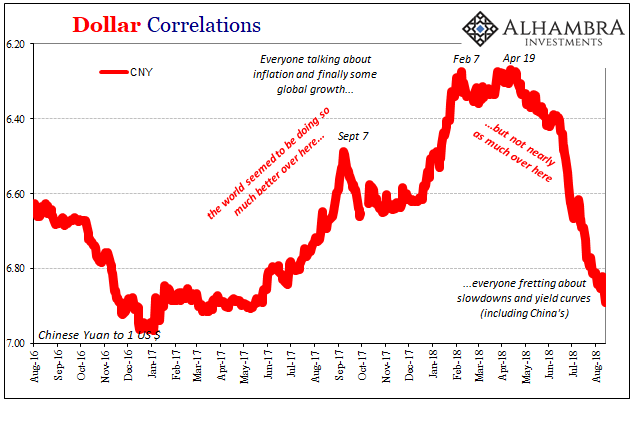

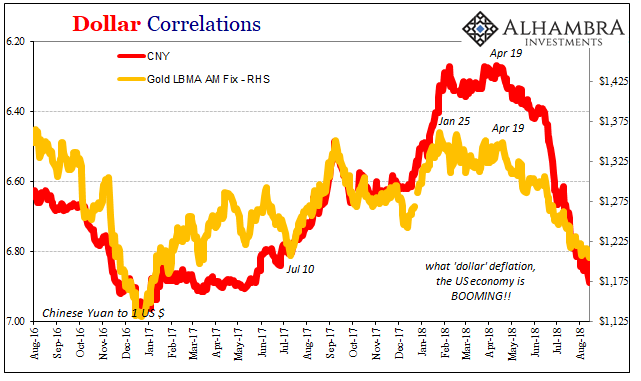

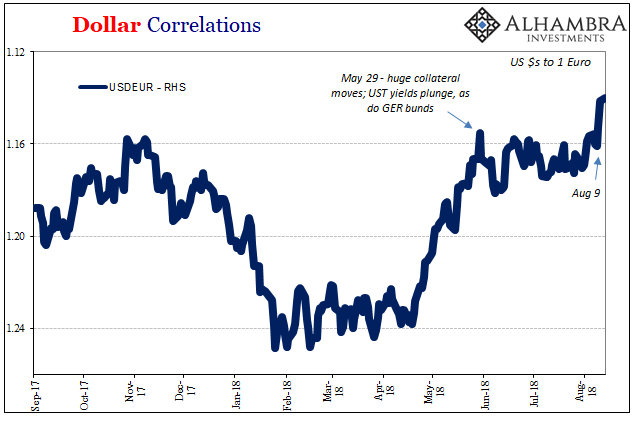

Complacency may be rampant again today, but CNY is dropping despite the now open presence of the PBOC to countermand that direction. Risk perceptions are rising, not falling (yield and eurodollar curves). And some key indications are right up against the edge of breaking out; the wrong way. Gold’s threatening to fall back into the $1,100’s, EUR is just about May 29 again, and DXY is already marginally higher.

It’s tragically too perfect that complacency disappeared again last week during the eleventh anniversary of August 9. Gold is still just barely hanging in the $1200’s, but I doubt for long. The euro was blasted into the 1.13’s, and DXY was for most of today closer to the 97’s than the 95’s.

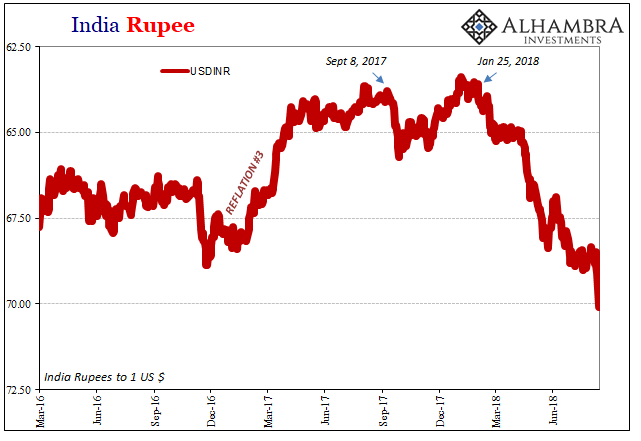

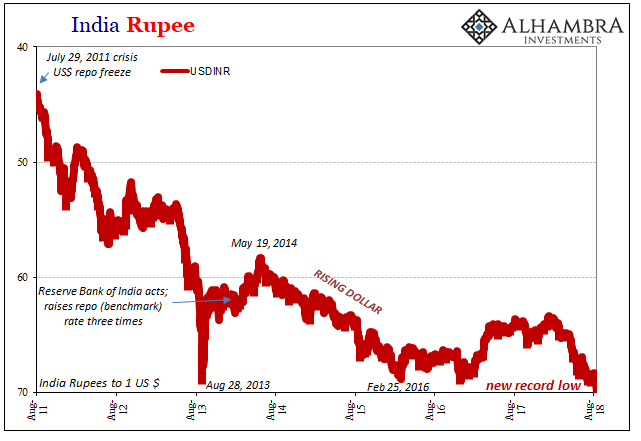

Among the EM’s, China’s yuan can’t find a stable range let alone price. The PBOC is there and it doesn’t help. India’s rupee has finally met 70, though I suspect Urjit Patel will have to go back to the Financial Times with some new reasons for this lamentable achievement.

More than either of those two of the BRIC’s we have to look again at Brazil. July was relatively good in that particular country; August not so much. The question is therefore what might have changed.

Leave A Comment