Call the Men in the White Coats Before it’s too Late

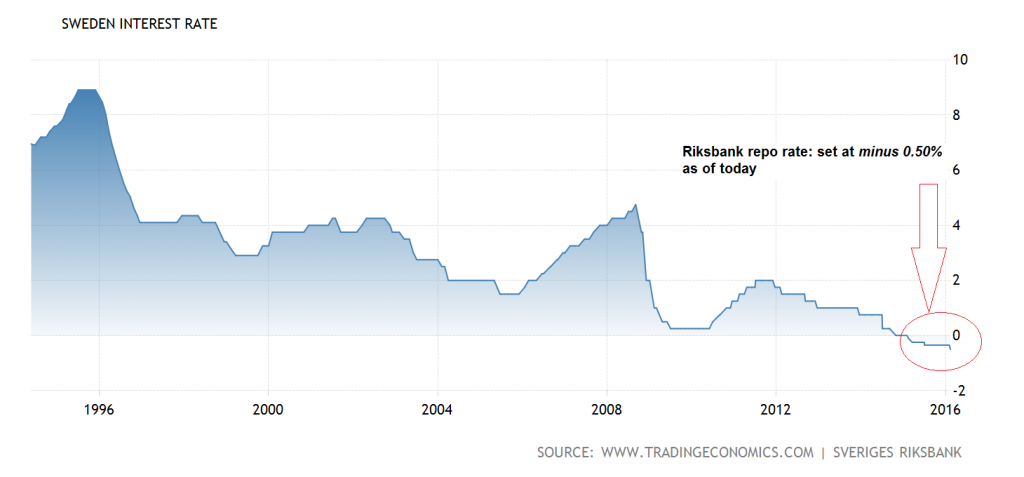

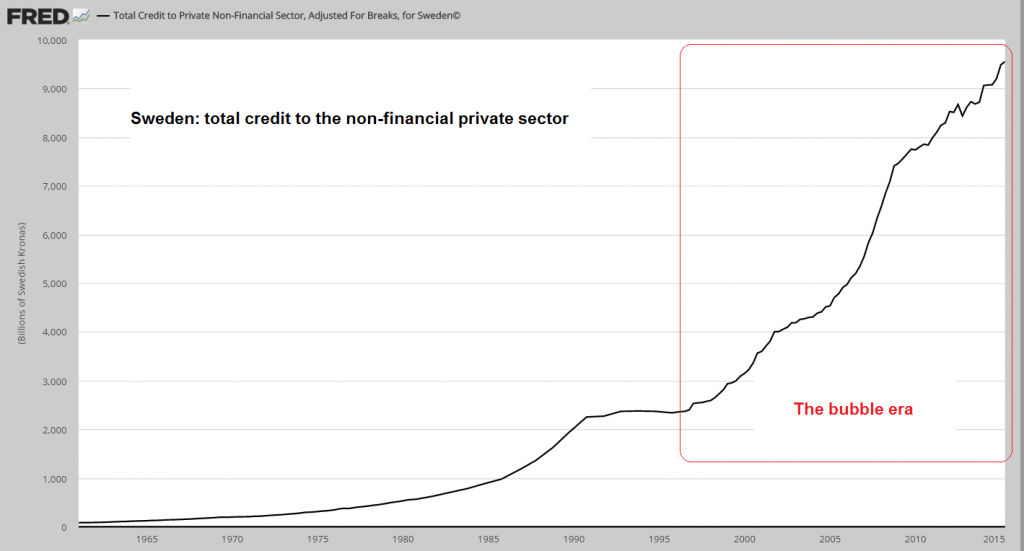

Today Sweden’s Riksbank “shocked the markets” by cutting its main refinancing rate further into negative territory, to minus 50 basis points. Note that according to the FT, “Sweden’s economy is booming”, and the Riksbank itself “forecasts that economic growth will be 3.5 per cent this year, a little lower than the 3.7 per cent in 2015”. Sweden also happens to be home to credit and real estate bubbles that are among the biggest on the planet.

Sweden’s central bank governor Stefan Ingves: yet another dangerous monetary quack

Photo credit: Thommy Tengborg / TT via AP

We hereby nominate the governor of the Riksbank Stefan Ingves for the “Upper Class Twit of the Year” award. We also urge all the good people in Sweden whose brains are not totally addled yet to quickly call for the men in white coats and have him committed before he can do even more damage.

Sweden’s central bank goes full retard by setting the repo rate at minus 50 bps, and promising even further cuts! – click to enlarge.

As we have pointed out many times, negative interest rates are an abomination. They could not possibly exist in a free market, unless the universe were to contract and arrow of time were to reverse. It is an apodictic certainty that the imposition of negative rates will lead to malinvestment, capital consumption, and ultimately impoverishment. So what gives? Why would the Swedish central bank lower rates even further into negative territory in the face of 3.5% GDP growth and raging credit and property bubbles?

Sweden’s raging credit bubble: total credit to the non-financial private sector – click to enlarge.

Monetary Quackery

The AP reports:

“Sweden’s central bank, worried about a long period of low inflation, decided Thursday to cut its key interest further below zero to a record minus 0.50 percent — and didn’t rule out further action.

Describing it as a “uniquely low interest rate,” Riksbank Governor Stefan Ingves didn’t want to speculate on future measures but said that “unfortunately the world looks different to what it did in December,” when the bank last discussed the economic situation. He pointed to a further drop in oil prices, turmoil in global markets and Japan’s decision last week to cut one of its key rates into negative territory, which has pushed down the yields payable on its bonds.

“The period of low inflation will be longer than we expected, increasing the risk of weakening confidence in the inflation target … and (of) inflation not rising toward the expected target,” of some 2 percent in 2017, Ingves said.”

Leave A Comment